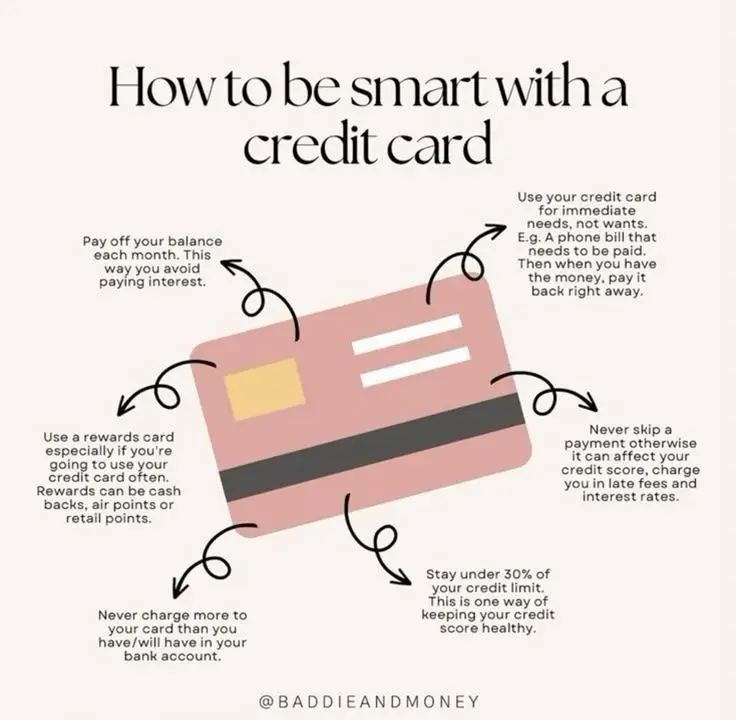

Pay Off Your Balance Each Month

One of the simplest yet most powerful habits you can develop with a credit card is paying off your balance in full every month. It sounds straightforward, but many people underestimate just how much this single habit can impact their financial life.

Why Paying in Full Matters

Credit cards are essentially short-term loans. When you use your card, the credit company lends you money, which you promise to repay later. If you don’t pay off the balance in full, the credit card company charges you interest on the remaining balance. And credit card interest rates are notoriously high—sometimes upwards of 20–30% annually.

Here’s a quick example: Imagine you spend $1,000 on your card and only pay the minimum—say $25—every month. The remaining balance accrues interest. Over time, that $1,000 can balloon to well over $1,200 or more, depending on your card’s interest rate. Suddenly, that small purchase is costing you far more than you intended.

By paying the full balance each month, you avoid these interest charges entirely. You’re effectively using your card for convenience and record-keeping, not for borrowing money you don’t have.

Benefits Beyond Avoiding Interest

Paying in full isn’t just about avoiding interest—it also has other significant benefits:

- Improved Financial Freedom: Not carrying a balance means you aren’t constantly worrying about growing debt. This can reduce stress and give you more control over your finances.

- Better Credit Score: Consistently paying in full shows lenders that you are responsible with credit. This behavior is recorded in your credit history and positively impacts your credit score.

- Budget Awareness: Paying off your balance each month forces you to track your spending, making you more aware of where your money goes.

Tips for Paying Off Your Balance

- Track Your Spending: Use your bank’s app or a budgeting tool to monitor your transactions in real time. Knowing exactly what you’ve spent helps you ensure you can pay the balance in full.

- Set Up Alerts: Many credit card companies allow you to set alerts when you approach your statement date or exceed a certain spending threshold. This keeps you accountable.

- Automate Payments: If remembering due dates is tricky, set up automatic full payments from your bank account each month. This guarantees you never miss a payment.

- Plan for Big Purchases: If you know you’ll need to make a large purchase, make sure it’s within your budget to pay it off immediately. Don’t let it linger and accumulate interest.

The Mindset Shift

Many people view credit cards as “extra money” they can borrow, but in reality, the smartest credit card users see them as tools for convenience and rewards—not free money. Paying off the balance each month requires discipline, but it’s the single most effective habit for preventing debt and building financial health.

Use Your Credit Card for Immediate Needs, Not Wants

Using a credit card wisely isn’t just about paying off your balance—it’s also about what you choose to charge in the first place. One of the most common mistakes people make is using their credit cards to buy things they want impulsively, rather than spending on what they actually need.

Needs vs. Wants: Understanding the Difference

Before swiping your card, it’s essential to distinguish between needs and wants:

- Needs are essential expenses that you must cover to maintain your day-to-day life. Examples include:

- Utility bills (electricity, water, internet)

- Phone bills

- Groceries

- Transportation costs

- Medical expenses

- Wants are non-essential items that are nice to have but not necessary for survival or financial stability. Examples include:

- Eating out at restaurants

- Designer clothes or accessories

- Gadgets you don’t immediately need

- Luxury vacations

Using your credit card primarily for needs keeps your spending responsible and prevents you from accumulating unnecessary debt.

Why Charging Only Needs Works

When you use your credit card for immediate needs rather than impulsive wants:

- You Reduce Impulsive Spending: Charging wants can lead to overspending because it’s easy to forget how much you’ve spent. Focusing on needs keeps your spending aligned with your budget.

- You Can Pay Off Your Balance Easily: Essentials are predictable costs. When you charge only things you know you need, you’re better positioned to pay off the balance in full.

- You Build a Healthy Financial Habit: This disciplined approach teaches you to think carefully before each swipe, creating long-term financial mindfulness.

Example: How to Apply This in Real Life

Let’s say your phone bill of $80 is due this month, and you only have cash in your bank for essentials. You can charge the bill to your credit card and then pay it off immediately once you receive your paycheck.

Contrast this with buying a $500 gadget just because it looks cool. Even if you pay it off later, you’ve spent money that could have gone toward essentials or savings—and you’ve risked carrying a balance with interest if things get tight.

Tips to Stick to Needs-Only Spending

- Plan Your Monthly Expenses: Write down all your necessary bills and purchases. This creates a clear picture of what your credit card should be used for.

- Separate Cards if Needed: Some people find it helpful to have one card strictly for essentials and another for discretionary spending. This visual separation helps control temptation.

- Set Spending Limits: Decide in advance the maximum amount you’ll spend on wants each month, if at all. Stick to it like a budget rule.

- Track Your Transactions Daily: Even small impulse charges can add up. Logging each transaction keeps you aware of your total spending.

The Long-Term Benefit

By using your credit card for needs, you’re essentially turning your credit card into a tool for convenience and financial tracking, rather than a temptation trap. Over time, this habit reduces stress, prevents debt accumulation, and positions you as a disciplined credit user—a status that not only benefits your wallet but also improves your credit score.

Never Skip a Payment

One of the cardinal rules of smart credit card use is never skipping a payment. Missing even a single payment can have immediate and long-term consequences for your finances.

How Missed Payments Affect Your Credit Score

Your credit score is a numerical representation of your creditworthiness. Payment history is the single most important factor in calculating your score, often accounting for 35% of your total credit score.

- Late Payments: If you miss a payment, it’s recorded as “late” on your credit report. Even a 30-day late payment can lower your credit score significantly.

- Repeated Misses: Habitual late payments signal to lenders that you are a high-risk borrower, making it harder to secure loans or credit in the future.

- Impact on Interest Rates: A lower credit score can lead to higher interest rates on loans or new credit cards, costing you more money in the long run.

The Cost of Late Fees and Interest

Skipping a payment doesn’t just hurt your credit score—it also adds direct costs:

- Late Fees: Most credit cards charge a late fee ranging from $25 to $40 per missed payment.

- Interest Rate Increases: Some credit cards increase your APR (annual percentage rate) if you miss a payment, meaning future balances will accrue more interest.

- Compounding Costs: If you carry a balance after missing a payment, the interest can grow quickly, turning a small mistake into a significant financial burden.

Here’s a practical example:

Imagine you have a $1,000 balance with a 20% interest rate. If you skip a $50 payment, you might be charged a $35 late fee, and the interest on the remaining balance continues to accrue. Before you know it, your debt could easily surpass $1,100—just from one missed payment.

Strategies to Avoid Missing Payments

- Set Up Autopay: Many credit cards allow you to schedule automatic full or minimum payments from your bank account. This ensures you never miss a due date.

- Use Calendar Reminders: If you prefer manual payments, set multiple reminders in your phone or digital calendar a few days before the due date.

- Check Statement Dates: Be aware of your statement closing and payment due dates. Planning around these dates can prevent accidental misses.

- Keep an Emergency Buffer: Even if you rely on credit cards for essential purchases, always maintain a small cash buffer in your bank account to cover unexpected shortfalls.

Mindset Shift: Treat Payments as Non-Negotiable

Think of your credit card payment as a monthly financial obligation, not an optional expense. Missing a payment isn’t just about fees or interest—it’s about preserving your financial reputation. Just like paying rent or utilities, your credit card balance should always be treated as a non-negotiable priority.

By committing to never skip a payment, you maintain control over your finances, protect your credit score, and avoid the stress that comes from spiraling debt.

Keep Your Credit Utilization Under 30%

Another key habit for smart credit card use is managing your credit utilization ratio—the percentage of your total credit limit that you’re actually using. Keeping this ratio under 30% is a simple yet powerful way to maintain a healthy credit score.

What is Credit Utilization?

Credit utilization measures how much of your available credit you’re using at any given time. For example:

- If your credit card has a $5,000 limit and you’ve spent $1,500, your credit utilization is 30%.

- If you’ve spent $2,500, your utilization jumps to 50%.

Credit scoring models, like FICO and VantageScore, look at utilization as a key factor. High utilization signals financial risk to lenders—they might think you rely too heavily on credit.

Why Staying Below 30% Matters

- Protects Your Credit Score: Using more than 30% of your credit limit can lower your score, even if you pay your balance on time.

- Shows Responsible Credit Behavior: Lenders see low utilization as a sign you manage credit responsibly and aren’t overspending.

- Prevents Debt Accumulation: Staying under 30% encourages mindful spending and reduces the risk of overspending beyond your means.

Example of Credit Utilization Impact

Imagine two people with the same $5,000 credit limit:

- Person A charges $1,000 (20% utilization) and pays it off in full each month.

- Person B charges $4,000 (80% utilization) but also pays in full.

Even though both pay off their balances, Person A’s credit score is likely higher because low utilization signals financial discipline and lower risk.

Tips to Keep Utilization Low

- Track Spending Closely: Regularly check your card balance and compare it to your total credit limit.

- Use Multiple Cards Strategically: If you have multiple credit cards, spreading out purchases can help keep utilization low on each card.

- Request Credit Limit Increases: Increasing your credit limit (without increasing spending) automatically lowers your utilization ratio.

- Pay Mid-Cycle: Consider making payments before your statement closes. This reduces the balance reported to credit bureaus, keeping your utilization lower.

The Mindset: Credit Cards Are Tools, Not Cash

Many people think having a high credit limit gives them more spending power, but in reality, a high balance relative to your limit can harm your credit score. Viewing your credit card as a tool—used responsibly and strategically—helps you maintain control over your financial health.

By keeping your utilization under 30%, you strike a balance: you enjoy the convenience and rewards of credit cards without damaging your credit profile. Over time, this habit can significantly improve your score and make you a more attractive candidate for loans, mortgages, and better credit offers.

Never Charge More Than You Have

One of the most important rules of responsible credit card use is simple: never charge more than you actually have or will have in your bank account. While credit cards can feel like “free money,” treating them this way is a fast track to debt and financial stress.

The Danger of Overspending

Credit cards make it easy to buy things you can’t immediately afford. This convenience can quickly become a trap:

- Accumulating Debt: If you charge more than you can pay off, the remaining balance starts accruing interest. Over time, even small overspending can grow into large debt.

- Stress and Anxiety: Watching your debt grow can be stressful and impact your overall financial well-being.

- Credit Score Impact: Consistently maxing out your card or carrying high balances increases your credit utilization, which can lower your credit score.

Even small repeated overspending—like charging $50–$100 beyond what you have each month—can compound over time, leading to a cycle of debt that’s hard to escape.

Align Spending with Actual Funds

The safest way to use a credit card is to treat it like a short-term bridge between when you need to pay for something and when you have the funds to cover it.

Here’s how to practice this:

- Know Your Bank Balance: Before charging anything, check that you have—or will have—the money to pay it off immediately.

- Budget Your Spending: Create a monthly budget for essential expenses and discretionary purchases. Charge only what fits within your budget.

- Avoid Impulse Purchases: It’s easy to swipe for things you want but don’t need. Pause and ask yourself if it’s something you can pay off immediately.

- Use Alerts: Many banking apps allow you to set notifications when your available balance is low, preventing accidental overspending.

Real-Life Example

Imagine you have $300 in your bank account and a $1,000 credit card limit. You buy a $500 gadget thinking you’ll pay it off later. Unexpectedly, your paycheck gets delayed or other expenses pop up. Now, you’re forced to either carry a balance with high interest or delay payments—both of which create financial stress.

By only charging what you already have or can immediately cover, you maintain financial control, avoid interest, and reduce the risk of falling into a debt cycle.

The Mindset Shift

Think of your credit card as a financial tool, not a safety net for overspending. Smart users only charge what they can pay off—viewing the card as a convenience, a record-keeping tool, and a way to earn rewards, rather than a source of “extra cash.”

This mindset helps you maintain discipline, reduce unnecessary financial stress, and ensures that your credit card works for you, rather than the other way around.

Use a Rewards Card Wisely

Credit cards can do more than just make payments convenient—they can earn you rewards for your everyday spending. However, using a rewards card wisely is key to ensuring you benefit financially rather than harm your finances.

Types of Rewards Cards

There are several types of rewards programs, each offering unique benefits:

- Cashback Cards: These give a percentage of your spending back as cash. For example, a 2% cashback card means a $100 purchase earns you $2.

- Airline or Travel Cards: These cards earn air miles or points that can be redeemed for flights, hotels, or other travel perks.

- Retail or Store Points Cards: These allow you to earn points for purchases that can be redeemed at specific stores or online retailers.

Choosing the right rewards card depends on your spending habits. If you travel frequently, an airline card may make sense. If your spending is mostly groceries and bills, a cashback card could be more practical.

How to Maximize Rewards Without Overspending

Rewards cards can be a double-edged sword. People sometimes overspend just to earn points, which defeats the purpose. Here’s how to use rewards cards effectively:

- Charge Only What You Can Pay Off: Never spend more than you would normally just to earn points or cashback. The interest you’d pay on overspending will almost always outweigh any reward.

- Leverage Bonus Categories: Many cards offer higher rewards for specific categories, like groceries, gas, or dining. Plan your spending to maximize these bonuses, but only within your budget.

- Pay Off the Balance Monthly: Rewards are only valuable if you pay off your balance. Carrying a balance can erase any benefits due to high interest rates.

- Track Your Rewards: Keep an eye on your earned points or cashback to ensure they are credited correctly and redeemed before expiration.

Example of Smart Rewards Use

Suppose you spend $1,000 per month on essentials, and your card gives 2% cashback. That’s $20 back every month—$240 a year—without spending an extra dime. Compare this with overspending $1,500 to earn “bonus points” and paying $150 in interest. The overspending scenario clearly hurts your finances rather than helping.

Additional Tips for Rewards Cards

- Annual Fees: Some rewards cards have annual fees. Ensure the benefits outweigh the cost.

- Sign-Up Bonuses: Many cards offer sign-up bonuses, but make sure you can meet the spending requirements without overspending.

- Redemption Strategy: Understand how to redeem rewards efficiently. Some programs offer better value for certain types of redemption.

- Avoid Cash Advances: Many rewards cards treat cash advances differently, often with high fees and no rewards. Use them only if absolutely necessary.

The Mindset: Rewards Are a Bonus, Not a Goal

The smartest cardholders don’t chase points—they focus on responsible spending first. Rewards should be seen as a bonus for disciplined financial behavior, not an incentive to overspend or carry debt. When used wisely, a rewards card can save money, provide perks, and even make your everyday purchases more enjoyable.

Additional Smart Credit Card Habits

Beyond the core rules of paying your balance, avoiding overspending, and using rewards wisely, there are several additional habits that can significantly improve your credit card management and financial health. These are the little practices that separate responsible credit users from those who struggle with debt.

1. Regularly Review Statements for Errors and Fraud

Even if you are disciplined with spending, mistakes can happen. Credit card companies sometimes make errors, and unfortunately, fraud is always a possibility.

- Check Transactions Monthly: Review each transaction on your statement carefully. Look for any unauthorized charges, duplicate billing, or unusual activity.

- Report Issues Immediately: If you spot errors or fraudulent charges, report them to your credit card company right away. Most companies have zero-liability policies for fraud, but timely reporting is essential.

- Keep Digital Records: Save your statements digitally or in a folder so you can reference them later if disputes arise.

2. Avoid Cash Advances Unless Absolutely Necessary

Cash advances—using your credit card to withdraw cash—come with high fees and interest rates. Unlike regular purchases, interest usually starts accruing immediately, and rewards are typically not earned.

- Use cash advances only as a last resort in emergencies.

- Explore alternatives like personal loans or borrowing from savings, which are often cheaper.

3. Set Personal Credit Limits and Alerts

Even if your card has a high credit limit, it doesn’t mean you should spend up to that limit.

- Set Your Own Limits: Decide on a personal maximum for monthly spending, separate from your official credit limit.

- Use Alerts: Many credit cards allow you to set alerts when spending reaches a certain threshold. This prevents accidental overspending.

- Break Large Expenses Into Smaller Payments: If possible, split big purchases over several months to manage cash flow without maxing out your card.

4. Plan for Large Expenses Strategically

When you need to make a big purchase, plan in advance:

- Time Your Purchase: Buy items just after your statement closes to give yourself maximum time to pay off the balance.

- Ensure Funds Are Available: Make sure you can pay the full amount when the bill arrives.

- Check for Rewards Opportunities: If you have a rewards card, see if the purchase qualifies for bonus points or cashback.

5. Maintain a Healthy Credit History

Even with perfect payment habits, neglecting your credit history can hurt your score.

- Keep Old Cards Open: The age of your credit accounts contributes to your credit score. Avoid closing old, unused accounts unless necessary.

- Diversify Credit Types: Having different types of credit (credit card, installment loan) can positively impact your score.

- Avoid Frequent Credit Applications: Every time you apply for new credit, it can slightly lower your score temporarily. Be selective.

6. Educate Yourself About Your Card’s Terms

Many credit card holders never read the fine print. Understanding your card’s terms ensures you avoid unnecessary fees or pitfalls:

- APR and Penalty Rates: Know what your interest rate is for purchases, cash advances, and late payments.

- Rewards Rules: Some rewards expire, others have minimum redemption requirements.

- Fees: Be aware of annual fees, foreign transaction fees, and other charges.

The Mindset: Treat Your Credit Card as a Financial Tool

Smart credit card use isn’t just about rules—it’s about mindset and discipline. Your card should be a tool that works for you, helping manage cash flow, earn rewards, and build a strong credit profile. By practicing these additional habits, you minimize risk, protect your credit, and maximize the benefits of responsible card ownership.

Mastering Smart Credit Card Use

Credit cards, when used wisely, are powerful financial tools. They offer convenience, security, rewards, and the opportunity to build a strong credit history. However, without discipline, they can quickly turn into a source of stress, debt, and financial setbacks.

Throughout this guide, we’ve explored the key habits that separate responsible credit card users from those who struggle:

- Pay Off Your Balance Each Month: Avoid interest, reduce stress, and build a strong credit profile.

- Use Your Card for Needs, Not Wants: Focus spending on essentials to stay within budget and prevent unnecessary debt.

- Never Skip a Payment: Protect your credit score and avoid late fees or penalty APRs.

- Keep Credit Utilization Under 30%: Maintain a healthy credit score and signal responsible credit behavior to lenders.

- Never Charge More Than You Have: Avoid debt traps and stay financially disciplined.

- Use Rewards Cards Wisely: Maximize benefits without overspending; view rewards as a bonus, not a reason to spend more.

- Adopt Additional Smart Habits: Review statements, avoid cash advances, set personal limits, plan large purchases, and understand your card’s terms.

The Mindset Shift for Long-Term Success

At the heart of all these tips is a simple mindset shift: treat your credit card as a tool, not free money. Use it to streamline payments, earn rewards, and manage cash flow—but always within your means.

Financial discipline isn’t about restricting yourself—it’s about control and strategy. By consistently practicing these habits, you can:

- Avoid unnecessary debt and interest payments

- Build and maintain a high credit score

- Maximize rewards and financial perks

- Gain peace of mind and confidence in your financial decisions

Remember, the difference between a good and a bad credit card experience isn’t the card itself—it’s how you use it. Make your credit card work for you, not against you, and you’ll be setting yourself up for years of financial health, flexibility, and freedom.