Money can feel overwhelming. Between investments, retirement accounts, mortgages, insurance policies, and the endless advice online, it’s no wonder many people freeze up when it comes to managing their finances. But here’s the good news: you don’t need to be a Wall Street pro to make smart money moves.

In fact, personal finance can often be boiled down into simple rules of thumb — quick shortcuts that guide you toward better decisions without requiring you to pull out a calculator every five minutes.

Think of them like cheat codes in a video game. They’re not perfect, but they get you most of the way there with almost no effort. And over the long haul, using these rules consistently can be the difference between financial stress and financial freedom.

In this article, we’ll walk through 7 timeless money rules that cover everything from investing to mortgages to insurance. You’ll see how millionaires, financial planners, and everyday people use these shortcuts to stay on track. And most importantly, you’ll learn how to apply them in your own life starting today.

Ready? Let’s dive in.

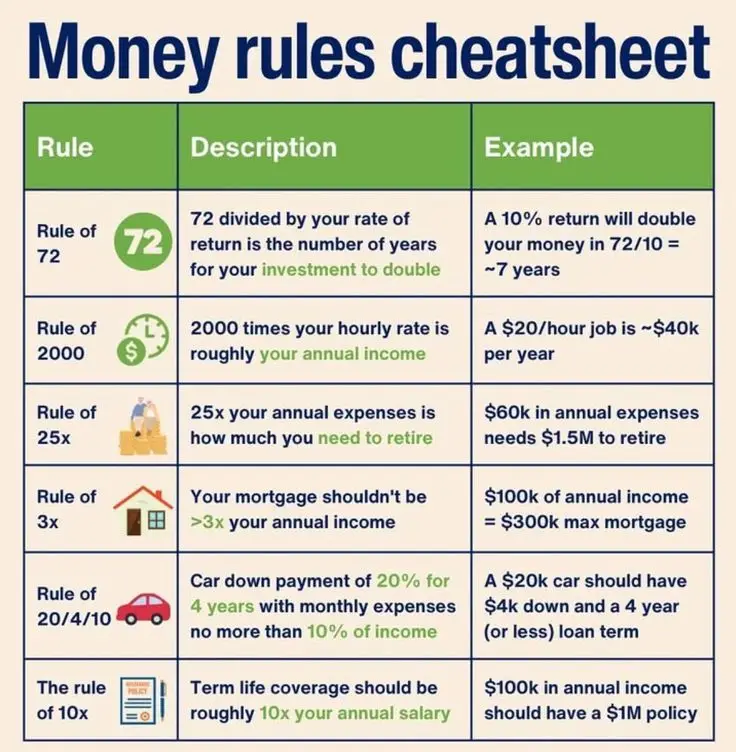

Part 1: The Rule of 72 – The Magic of Compounding

If there’s one money rule that will blow your mind, it’s this one. The Rule of 72 shows you just how fast your money can double with investing.

The formula is simple:

72 ÷ rate of return = years it takes to double your money.

That’s it.

Example in Action

- At 10% return, your money doubles in roughly 7 years.

- At 6% return, it doubles in 12 years.

- At 3% return, it takes 24 years.

So, if you invested $10,000 at 10% return, in 7 years you’d have $20,000, in 14 years you’d have $40,000, and in 21 years you’d have $80,000 — all without adding a single extra dollar.

Why This Rule Matters

- Compounding power – You start to see why investing early matters so much. The earlier you begin, the more doubling cycles you get.

- Inflation awareness – The rule also works in reverse. If inflation averages 3%, your money loses half its value in about 24 years.

- Quick comparison tool – Not sure if a 6% vs. 8% investment return is worth chasing? The Rule of 72 shows you the difference in doubling time instantly.

Real-Life Use

Let’s say you’re 25 years old with $10,000 invested at 8% return:

- By 32: $20,000

- By 39: $40,000

- By 46: $80,000

- By 53: $160,000

- By 60: $320,000

And that’s from just $10,000 left alone. Imagine if you kept adding contributions.

💡 The takeaway: Your money is either working for you or against you. The Rule of 72 shows you how fast wealth grows — or how fast inflation erodes it.

Part 2: The Rule of 2000 – Know Your Annual Income Instantly

The Rule of 2000 is a shortcut for converting your hourly wage into annual income.

Here’s how it works:

Hourly rate × 2000 ≈ Annual salary

This rule assumes you work about 40 hours a week, 50 weeks a year.

Example in Action

- $20/hour × 2000 = $40,000/year

- $30/hour × 2000 = $60,000/year

- $50/hour × 2000 = $100,000/year

Why This Rule Matters

- Negotiations – If you’re considering a new job and they’re offering $28/hour, you can instantly see it’s about $56k/year.

- Side hustles – Thinking about starting a gig that pays $25/hour? That’s roughly $50k/year if it were full-time.

- Reality check – Helps you quickly compare offers, hours, and the impact of raises.

Real-Life Use

If your boss offers a $2/hour raise, it doesn’t sound huge. But using the Rule of 2000, you see that’s about $4,000/year. Suddenly it feels a lot more valuable.

💡 The takeaway: Always know your annualized income. It’s the only way to plan budgets, savings, and investments realistically.

Part 3: The Rule of 25x – The Retirement Freedom Formula

This is the cornerstone of the FIRE movement (Financial Independence, Retire Early). The Rule of 25x tells you how much money you need to retire comfortably.

The formula is:

25 × annual expenses = retirement savings target.

Example in Action

- $40,000 expenses → need $1,000,000 to retire.

- $60,000 expenses → need $1,500,000.

- $100,000 expenses → need $2,500,000.

This comes from the “4% rule,” which says you can safely withdraw about 4% of your portfolio each year without running out of money.

Why This Rule Matters

- Clarity – Instead of wondering “Do I have enough to retire?” you get a concrete number.

- Motivation – Suddenly, cutting expenses has a direct payoff. If you reduce annual expenses by $10,000, you need $250k less saved.

- Goal setting – You can work backward to plan savings, investments, and timelines.

Real-Life Use

If you currently spend $50k a year and have $500k saved, you’re halfway to your retirement goal of $1.25M. That’s powerful to know.

💡 The takeaway: Retirement isn’t about age, it’s about math. Once your portfolio equals 25x expenses, you’re financially free.

Part 4: The Rule of 3x – A Smarter Mortgage Limit

Buying a home is one of the biggest financial decisions you’ll ever make. The Rule of 3x keeps you from getting in over your head.

The rule says:

Your mortgage shouldn’t be more than 3× your annual income.

Example in Action

- $80k annual income → max $240k mortgage.

- $100k income → max $300k mortgage.

- $150k income → max $450k mortgage.

Why This Rule Matters

- Bank traps – Lenders often approve you for much more, but that doesn’t mean you should take it.

- Budget breathing room – Housing should be comfortable, not crushing.

- Investment opportunity – A smaller mortgage frees up cash for investing.

Real-Life Use

Let’s say you earn $90k. The bank says you qualify for a $450k home, but the Rule of 3x suggests $270k. Choosing the smaller home could save you thousands per month — money that can grow wealth instead of servicing debt.

💡 The takeaway: A house should be a blessing, not a financial anchor. Follow 3x to stay safe.

Part 5: The Rule of 20/4/10 – Buying Cars Without Going Broke

Cars are sneaky wealth destroyers. The 20/4/10 Rule helps keep them in check.

Here’s the breakdown:

- Put 20% down.

- Finance for no more than 4 years.

- Keep total car costs under 10% of your income.

Example in Action

- A $20k car = $4k down, max 4-year loan, with payments + insurance + gas under 10% of income.

- If you make $60k/year, that means car expenses shouldn’t exceed $6k/year (or $500/month).

Why This Rule Matters

- Cars depreciate fast – Buying above your means traps you in debt for something losing value.

- Budget control – Keeps your car from eating into investing power.

- Freedom – A car should get you places, not keep you financially stuck.

Real-Life Use

If you earn $50k, your total monthly car costs should be $400 or less. That rules out most luxury vehicles — and that’s the point.

💡 The takeaway: Drive what fits your wallet, not your ego.

Part 6: The Rule of 10x – Protecting Your Family With Life Insurance

If others depend on your income, life insurance is non-negotiable. The Rule of 10x makes it easy:

Get term life insurance equal to 10× your annual salary.

Example in Action

- $60k income → $600k policy.

- $80k income → $800k policy.

- $100k income → $1M policy.

Why This Rule Matters

- Family protection – If you’re gone, your loved ones can continue living without financial chaos.

- Quick calculation – No need to overcomplicate with endless formulas.

- Cost-effective – Term life insurance is affordable, especially when bought young.

Real-Life Use

A 30-year-old making $75k can get a $750k term policy for about the cost of a weekly dinner out. Small price for peace of mind.

💡 The takeaway: Insurance isn’t for you — it’s for the people you love.

Part 7: Putting It All Together – Living by the Money Cheatsheet

These rules are powerful individually, but they’re game-changing when used together.

Imagine a 30-year-old making $70k/year applying all 7 rules:

- Invest early and watch money double with the Rule of 72.

- Calculate salary offers quickly with the Rule of 2000.

- Aim for $1.75M retirement savings with the Rule of 25x (if expenses are $70k).

- Buy a home under $210k with the Rule of 3x.

- Drive a car under $400/month all-in with the Rule of 20/4/10.

- Protect family with a $700k term policy using the Rule of 10x.

This person isn’t just making random financial decisions — they’re following a framework that builds long-term freedom.

Conclusion

Money doesn’t have to be complicated. These 7 simple rules give you a cheatsheet for smarter, faster financial decisions. They’re not perfect formulas, but they’ll keep you on track and protect you from some of the biggest money mistakes people make.

The key is to apply them consistently. Whether you’re negotiating pay, shopping for a car, or planning retirement, let these rules guide you.

So, which rule will you start with today? Even applying just one could make your financial life instantly clearer.