Most people grow up with one idea about money: you go to school, get a job, and earn a paycheck. That’s what we call earned income—and while it’s the most common type, it’s also the most limiting.

Wealthy people think differently. They don’t just work for money—they make money work for them. Instead of relying on one income stream, they diversify across multiple types.

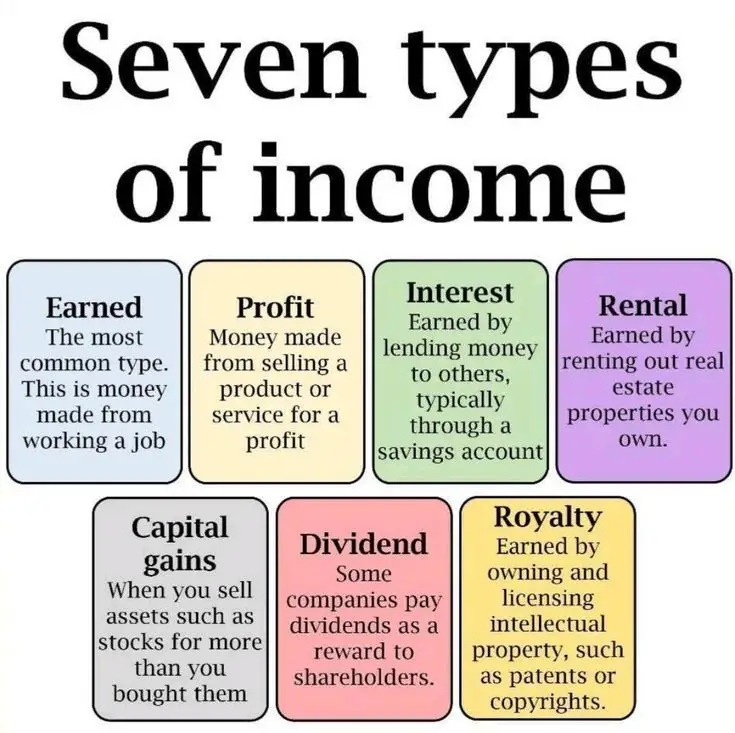

This article explores the 7 types of income, why they matter, and how you can start building them into your life.

1. Earned Income (Active Work)

This is the most familiar type of income: money you make by trading your time for money.

Examples

- Salary from a job

- Hourly wages

- Freelancing

- Side hustles like tutoring or delivery driving

Pros

- Predictable and stable.

- Entry-level, anyone can start here.

Cons

- Tied to time and effort.

- High taxes compared to other income types.

- If you stop working, income stops.

Case Study: Alex

Alex works a 9–5 earning $50,000/year. His income is steady, but capped—he only earns more if he works overtime or negotiates a raise.

How to Maximize Earned Income

- Build in-demand skills.

- Ask for raises based on measurable results.

- Use side hustles to supplement.

- Avoid lifestyle inflation—save the extra.

2. Profit Income (Business Ownership)

This is income from selling goods or services for more than they cost to produce.

Examples

- Running an online store (Shopify, Etsy).

- Owning a restaurant.

- Offering a service like consulting, coaching, or landscaping.

Pros

- Unlimited upside.

- You own the system, not just your time.

- Can eventually become passive if automated.

Cons

- Risk of failure.

- Requires upfront effort and sometimes capital.

Case Study: Maria

Maria started selling handmade jewelry online. At first, it was side money. But after refining her product line and using social media marketing, she scaled it into a six-figure business.

How to Start

- Test small with digital products or services.

- Keep overhead low at the beginning.

- Learn marketing—it drives sales.

3. Interest Income

This is money earned by lending money. You become the bank.

Examples

- Savings accounts (though rates are low).

- Certificates of deposit (CDs).

- Bonds.

- Peer-to-peer lending platforms.

Pros

- Relatively safe, especially with government-backed savings.

- Passive income once money is lent.

Cons

- Low returns compared to stocks or businesses.

- Vulnerable to inflation eating away value.

Case Study: John

John placed $50,000 in a high-yield savings account earning 4%. That generates $2,000/year in passive income without him lifting a finger.

How to Start

- Open a high-yield savings account.

- Ladder CDs for higher returns.

- Explore treasury bonds or money market accounts.

4. Rental Income

Money made from renting out property you own.

Examples

- Renting out apartments or houses.

- Airbnb or vacation rentals.

- Renting office space or storage units.

Pros

- Generates recurring monthly income.

- Property values often increase over time.

- Tax advantages (depreciation, write-offs).

Cons

- Requires large upfront capital or loans.

- Property management headaches.

- Vacancies or bad tenants reduce income.

Case Study: Priya

Priya bought a duplex and lived in one unit while renting out the other. The tenant’s rent covered her mortgage, letting her live nearly for free while her property grew in value.

How to Start

- House-hack (rent out part of your own home).

- Start with small, affordable properties.

- Hire a property manager if you want hands-off investing.

5. Capital Gains

This happens when you sell an asset for more than you bought it.

Examples

- Selling stocks, crypto, or ETFs.

- Selling a house at a profit.

- Flipping cars or collectibles.

Pros

- Can generate big payouts.

- Often taxed at lower rates than earned income.

Cons

- Not guaranteed—values can drop.

- Requires patience and good timing.

Case Study: Liam

Liam invested $20,000 in Apple stock. After holding for 10 years, it grew to $150,000. When he sold, he booked $130,000 in capital gains.

How to Start

- Learn about stock investing.

- Invest long-term, avoid chasing quick flips.

- Use tax-advantaged accounts to minimize taxes.

6. Dividend Income

Some companies share profits with shareholders in the form of dividends.

Examples

- Dividend-paying stocks (Coca-Cola, Johnson & Johnson).

- REITs (real estate investment trusts).

- Mutual funds or ETFs focused on dividends.

Pros

- Passive and recurring.

- Great for retirement income.

- Can be reinvested for compounding.

Cons

- Dividend stocks can still lose value.

- Companies can cut dividends.

Case Study: Rachel

Rachel invested $100,000 in a dividend ETF paying 4%. That gives her $4,000/year—enough to cover vacations or groceries—without selling any shares.

How to Start

- Open a brokerage account.

- Research dividend aristocrats (companies that have raised dividends for 25+ years).

- Reinvest dividends until you need the cash flow.

7. Royalty Income

This is income from owning intellectual property. You create something once, and get paid every time it’s used.

Examples

- Book royalties.

- Music licensing.

- Patents.

- Online courses or digital products.

Pros

- Scalable: create once, earn many times.

- Potential for global reach.

- Passive after initial creation.

Cons

- Hard to build at first.

- Requires creativity or expertise.

- Income can be unpredictable.

Case Study: Daniel

Daniel wrote an e-book on personal finance and published it on Amazon. At first, sales were slow, but over 5 years it generated $50,000 in royalties—while he worked his day job.

How to Start

- Write and self-publish an e-book.

- License your photography or music.

- Build digital products that solve problems.

Bringing It All Together

The seven types of income can be grouped into active vs passive:

- Active: Earned, Profit

- Passive (or semi-passive): Interest, Rental, Capital Gains, Dividend, Royalty

Most people start with earned income and maybe dabble in profit income through side hustles. The wealthy, however, build multiple streams of passive income that eventually exceed their active income.

Final Thoughts

If you rely only on a paycheck, your financial growth will always be limited. By diversifying into multiple income types, you create:

- Stability (if one income dries up, others keep flowing).

- Growth (capital gains and dividends build wealth).

- Freedom (passive income gives you time back).

You don’t need all 7 today. But by age 30, if you’ve mastered earned income and added even one or two passive income streams, you’re already ahead.

The ultimate goal? Build income that works even when you don’t. That’s the real path to financial independence.