Wealth isn’t built overnight. It isn’t luck, and it isn’t reserved for the chosen few. It’s a system—a structure of decisions and habits that compound over time.

If you study the lives of financially successful people, you’ll notice a repeating pattern: they don’t just earn money—they manage it, protect it, grow it, and pass it on.

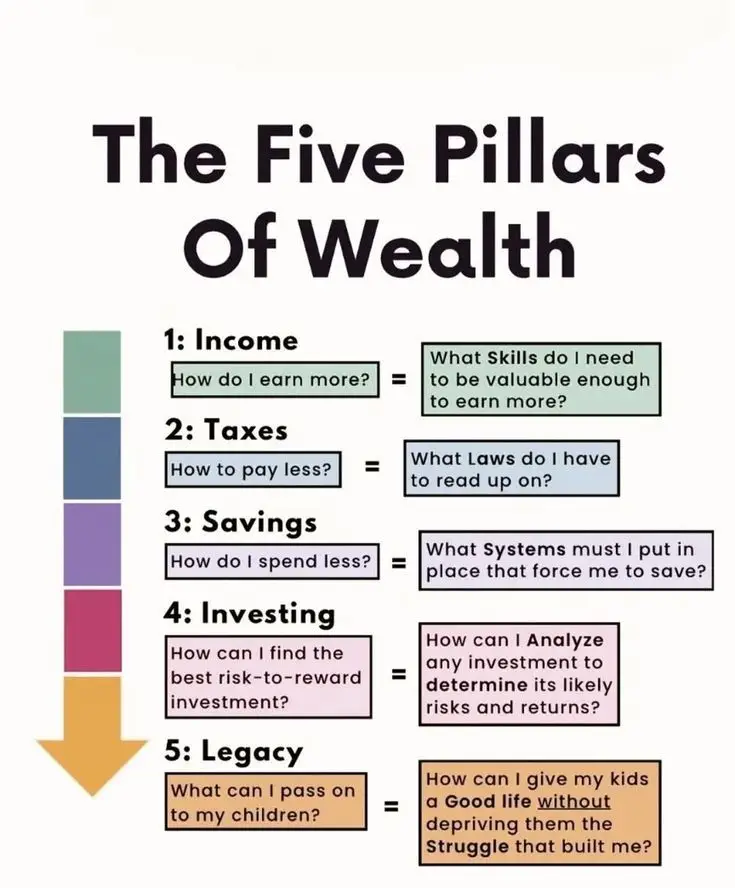

That’s why true wealth rests on five solid foundations:

- Income – The fuel that drives everything.

- Taxes – Keeping more of what you earn.

- Savings – Protecting your financial foundation.

- Investing – Growing your money over time.

- Legacy – Leaving wealth, wisdom, and values behind.

These five pillars form a holistic wealth-building system. Let’s explore each in detail, with actionable steps, examples, and strategies that can transform your financial life.

Pillar 1: Income – Building the Engine of Wealth

Money starts here. Income is the raw material that fuels your financial journey. Without it, there’s nothing to save, invest, or pass down.

But here’s the thing: it’s not just about earning more—it’s about earning smarter.

The Key Question:

“What skills do I need to be valuable enough to earn more?”

Why Income Matters

- Income sets the pace of your financial growth.

- It determines how quickly you can save and invest.

- It gives you options—better healthcare, housing, education, and freedom.

Ways to Increase Income

- Increase Your Value at Work

- Learn high-demand skills: coding, data analytics, AI, digital marketing, project management.

- Seek leadership roles or specialized expertise.

- Ask for raises backed by results, not just time served.

- Create Additional Income Streams

- Freelancing or consulting in your expertise.

- Starting a side business (e-commerce, digital products, content creation).

- Investing in real estate rentals or dividend stocks.

- Leverage Technology

- Create assets that scale: courses, apps, YouTube channels, e-books.

- Use platforms like Upwork, Etsy, or Shopify to reach a global audience.

Case Study: Sarah the Graphic Designer

Sarah earned $50,000/year as a full-time designer. She realized she could earn more by:

- Learning UX/UI design → raised her value to employers.

- Taking freelance clients on weekends → extra $1,000/month.

- Selling design templates on Etsy → $500 passive income/month.

Within 2 years, her total income doubled to $100,000+.

Mindset Shift

Stop trading time for money. Start trading value for money. The more value you create, the more income you’ll generate.

Pillar 2: Taxes – Keeping More of What You Earn

Making money is half the battle. Keeping it is the other half. For most people, taxes are the largest expense in their lifetime.

The Key Question:

“What laws do I have to read up on?”

Why Taxes Matter

- You can’t build wealth if you give away too much unnecessarily.

- Wealthy people don’t evade taxes—they master tax strategy.

Ways to Pay Less (Legally)

- Understand Your Tax Bracket

- Know how much of your income is taxed at different levels.

- Avoid accidentally pushing yourself into higher brackets with poor planning.

- Max Out Tax-Advantaged Accounts

- 401(k), 403(b), 457 → Pre-tax contributions lower taxable income.

- Roth IRA → Future withdrawals are tax-free.

- HSA → Triple tax advantage (deductible, tax-free growth, tax-free withdrawals).

- Leverage Business Structures

- Freelancers and entrepreneurs can use LLCs or S-Corps.

- Deduct business expenses: home office, internet, software, travel, equipment.

- Use Deductions and Credits

- Child tax credit, education credits, energy-efficient home upgrades.

- Student loan interest, mortgage interest.

Case Study: David the Freelancer

David earned $80,000 as a freelance consultant. He:

- Formed an LLC and wrote off his laptop, internet, and part of his rent.

- Contributed $6,000 to a Traditional IRA (lowering taxable income).

- Put $3,000 into an HSA.

Result: He legally saved over $10,000 in taxes in one year.

Mindset Shift

Don’t just think about how much you make—think about how much you keep. Every dollar saved in taxes is a dollar that can be invested.

Pillar 3: Savings – Protecting Your Future Self

Earning more means little if you spend it all. Savings is the discipline that turns income into long-term wealth.

The Key Question:

“What systems must I put in place that force me to save?”

Why Savings Matter

- Protects against emergencies.

- Prevents debt when unexpected expenses arise.

- Builds the foundation for investing.

The Savings System

- Emergency Fund

- 3–6 months of living expenses in a high-yield savings account.

- This is your financial safety net.

- Sinking Funds

- Mini savings accounts for planned but irregular expenses (car repairs, vacations, holidays).

- Automation

- Set automatic transfers from checking to savings every payday.

- Treat savings as a bill—non-negotiable.

Case Study: Anna the Teacher

Anna earned $45,000/year. She struggled to save because she relied on willpower. Once she automated $300/month into a high-yield savings account, she built a $10,000 emergency fund in less than 3 years—without stressing about it.

Mindset Shift

Saving isn’t about deprivation—it’s about freedom. Every dollar saved buys peace of mind and future options.

Pillar 4: Investing – Making Money Work for You

If income is the engine and savings is the safety net, investing is the rocket fuel. Savings alone won’t build lasting wealth—you must invest.

The Key Question:

“How can I analyze any investment to determine its likely risks and returns?”

Why Investing Matters

- Inflation erodes cash.

- Investments compound wealth over time.

- Investing creates passive income streams.

Types of Investments

- Stocks

- Ownership in companies.

- High long-term returns (~7–10% historically).

- Bonds

- Loans to governments or companies.

- Lower risk, lower returns.

- Real Estate

- Rental income + property appreciation.

- Tangible asset, tax benefits.

- Businesses

- Starting or owning part of a business.

- High risk, high reward.

- Alternative Investments

- REITs, commodities, private equity, crypto (higher risk).

Case Study: Mark the Engineer

Mark invested $500/month in an S&P 500 index fund starting at age 25. By age 55, he had over $600,000. By retirement, it grew to over $1.2 million—just from consistency.

Mindset Shift

Don’t let fear stop you from investing. The biggest risk isn’t losing money—it’s never starting.

Pillar 5: Legacy – Building Wealth Beyond Yourself

Wealth is about more than money—it’s about impact. Legacy is the mark you leave on your family, community, and the world.

The Key Question:

“How can I give my kids a good life without depriving them of the struggle that built me?”

Why Legacy Matters

- Provides generational security.

- Teaches values and financial literacy.

- Ensures your hard work lives on.

How to Build Legacy

- Estate Planning

- Write a will.

- Use trusts to avoid probate and protect assets.

- Name beneficiaries on all accounts.

- Teach Financial Literacy

- Involve kids in budgeting and investing.

- Teach them about money early, not when they’re already in debt.

- Pass on Values

- Show resilience, discipline, generosity.

- Legacy isn’t just money—it’s mindset.

- Philanthropy

- Donate to causes you care about.

- Set up scholarships or community programs.

Case Study: Maria the Business Owner

Maria built a successful restaurant business. Instead of just leaving money to her children, she:

- Created a family trust for financial assets.

- Trained her kids to run the business.

- Donated 10% of profits to local food banks.

Her legacy wasn’t just wealth—it was empowerment and impact.

Mindset Shift

Legacy is not about spoiling your kids. It’s about preparing them. Give them a head start, not a free ride.

Bringing It All Together

The Five Pillars of Wealth form a complete system:

- Income → You earn.

- Taxes → You keep.

- Savings → You protect.

- Investing → You grow.

- Legacy → You pass on.

Neglect one, and the system weakens. Strengthen all five, and you’ll create a financial life that not only supports you now, but also builds a future for generations to come.

Final Thoughts

Wealth is not about luck, or greed, or working yourself into exhaustion. It’s about building wisely, step by step, with intention.

Start with income. Protect it with tax knowledge. Guard it with savings. Multiply it through investing. And, ultimately, pass it on with purpose.

If you do that, you won’t just build money—you’ll build freedom, security, and a lasting legacy.