Most of us grow up with one lesson drilled into our heads: work hard, earn money, and spend carefully. But here’s the truth — earning money is only the first step in financial success. The real journey begins with learning how to budget wisely and then expanding income streams beyond just a paycheck.

In this guide, we’ll break things down into two parts:

- How to Budget on a Low Income – Practical steps anyone can take to take control of their money, even if funds feel tight.

- The Seven Types of Income – A roadmap to building wealth and financial independence by diversifying how money flows into your life.

Whether you’re just starting out, living paycheck to paycheck, or dreaming of long-term wealth, this article will walk you through strategies that actually work.

Part 1: How to Budget on a Low Income

Budgeting doesn’t have to be restrictive. Think of it like giving every dollar a job so you know where it’s going instead of wondering where it went. And yes—even with a low income, you can save and make progress toward financial stability.

Here’s how.

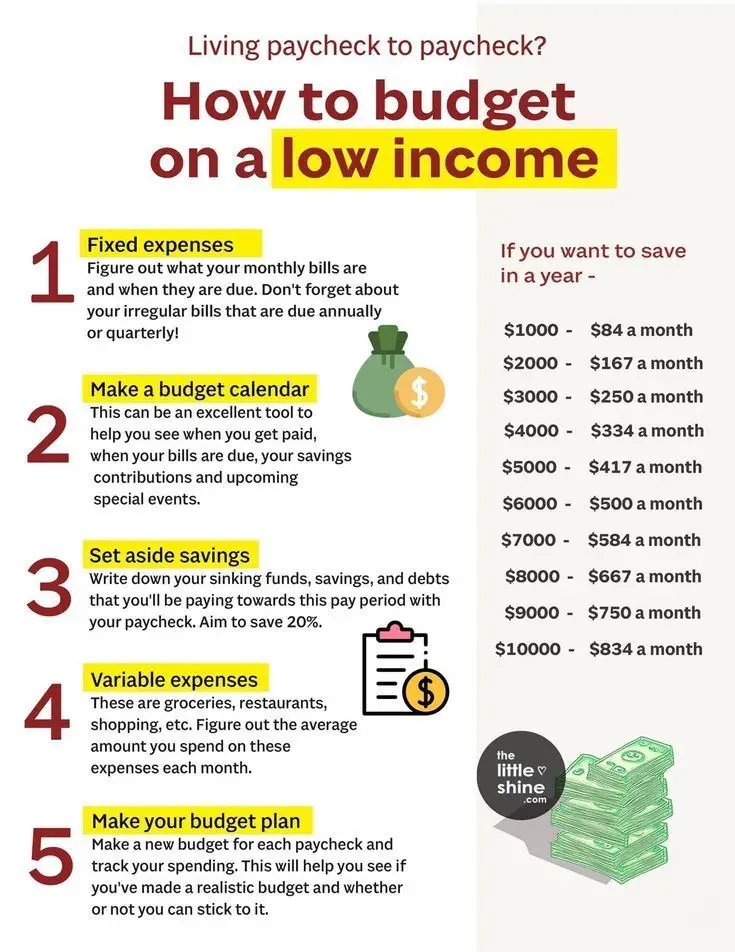

Step 1: Identify Fixed Expenses

Fixed expenses are the bills you must pay every month. These usually stay the same and include things like:

- Rent or mortgage payments

- Utilities (electricity, water, internet, phone)

- Insurance premiums (car, health, renter’s/homeowner’s)

- Loan payments (student loans, car loans, credit cards minimums)

Why is this step so important? Because knowing exactly what you owe—and when—removes financial surprises. Many people struggle not because they don’t earn enough, but because they don’t know when their bills are due.

👉 Tip: Write down each fixed expense, its amount, and its due date. If some bills are quarterly or annual (like car insurance or property tax), divide the cost by 12 and set aside a little each month. This keeps you prepared instead of scrambling later.

Step 2: Make a Budget Calendar

Once you know your fixed expenses, it’s time to map them out against your paycheck schedule. This is where a budget calendar comes in handy.

A budget calendar shows:

- When you get paid

- When each bill is due

- When savings contributions happen

- Any upcoming special events (birthdays, holidays, vacations)

This lets you see cash flow at a glance. For example, if you know your rent and car payment are due right after payday, you won’t overspend that week.

👉 Tip: You can use a physical wall calendar, a planner, or a free budgeting app like YNAB, Mint, or even Google Calendar. The key is to be consistent.

Step 3: Set Aside Savings

Here’s the golden rule: Pay yourself first.

Even on a tight income, savings must come before spending. Why? Because if you wait until the end of the month to save “whatever’s left,” chances are—nothing will be left.

Aim to save 20% of your paycheck. If that feels impossible right now, start smaller—5% or even 1%. What matters is building the habit.

This money can go into:

- Emergency fund (at least $1,000 to start, then 3–6 months of expenses)

- Sinking funds (for future expenses like car repairs, vacations, holiday shopping)

- Investments (retirement accounts or brokerage)

👉 Tip: Automate savings. Have your employer split your direct deposit so part goes straight into savings, or set up automatic transfers on payday.

Step 4: Track Variable Expenses

Variable expenses are the ones that fluctuate month to month. These include:

- Groceries

- Gas

- Eating out

- Shopping

- Entertainment

These are often the “budget killers” because they sneak up on us. Tracking them helps you identify patterns.

👉 Tip: Use the “cash envelope” system or a digital version (apps like Goodbudget). Give yourself a set amount for groceries, restaurants, and entertainment—and once it’s gone, it’s gone.

Step 5: Make a Realistic Budget Plan

Every paycheck deserves a new plan. Why? Because life changes. You may have an extra bill one month, or maybe you got a small bonus. By planning paycheck by paycheck, you stay flexible and realistic.

Common Budgeting Mistakes to Avoid

- Being too strict. If your budget feels suffocating, you won’t stick to it.

- Forgetting irregular expenses. That annual car registration fee shouldn’t be a surprise.

- Not tracking. If you don’t measure, you can’t improve.

Budgeting isn’t about perfection. It’s about awareness.

Yearly Savings Goals (The Table)

Here’s how much you need to save each month to hit different annual savings targets:

- $1,000 → $84 per month

- $2,000 → $167 per month

- $3,000 → $250 per month

- $4,000 → $334 per month

- $5,000 → $417 per month

- $6,000 → $500 per month

- $7,000 → $584 per month

- $8,000 → $667 per month

- $9,000 → $750 per month

- $10,000 → $834 per month

👉 Example: Want to save $5,000 this year? That’s about $417 per month, or $14 a day. Suddenly, the goal feels less overwhelming.

Part 2: The Seven Types of Income

Now that you know how to control and manage your money, the next step is growing your income streams.

Most people rely only on earned income (a paycheck). The wealthy, however, diversify across multiple sources. Let’s break down the seven types of income and how you can start building them.

1. Earned Income (Trading Time for Money)

The most common type—money you get from working a job.

Examples: salary, hourly wages, freelancing, side hustles.

Pros: Reliable, beginner-friendly.

Cons: Limited, stops when you stop working.

👉 How to grow it: Learn high-demand skills, negotiate raises, start freelancing.

2. Profit Income (Business Ownership)

Money earned when you sell something for more than it costs you.

Examples: online store, consulting, selling digital products.

Pros: Unlimited upside, scalable.

Cons: Risky, requires effort.

👉 How to start: Launch a side hustle. Test an idea with low overhead before going big.

3. Interest Income (Lending Money)

You become the bank and earn interest.

Examples: savings accounts, CDs, bonds, peer-to-peer lending.

Pros: Safe, passive.

Cons: Lower returns, inflation risk.

👉 How to start: Open a high-yield savings account, buy government bonds.

4. Rental Income (Owning Property)

Money from renting out real estate.

Examples: apartments, Airbnbs, office space.

Pros: Recurring income, property value grows.

Cons: Upfront capital needed, management headaches.

👉 How to start: Try “house hacking”—renting out part of your own home.

5. Capital Gains (Selling Assets for Profit)

Money you make when you sell something for more than you paid.

Examples: stocks, crypto, real estate, collectibles.

Pros: Can generate big wealth, tax-advantaged.

Cons: Risk of loss, requires patience.

👉 How to start: Open a brokerage account, focus on long-term investing.

6. Dividend Income (Owning Stocks That Pay You)

Certain companies share profits with investors via dividends.

Examples: dividend-paying stocks, ETFs, REITs.

Pros: Passive, recurring, great for retirement.

Cons: Companies can cut dividends, stock prices fluctuate.

👉 How to start: Invest in dividend “aristocrats”—companies that have raised dividends for decades.

7. Royalty Income (Owning Intellectual Property)

You earn money when people use something you created.

Examples: books, music, patents, online courses.

Pros: Scalable, passive after creation.

Cons: Hard to build, unpredictable.

👉 How to start: Write an e-book, create digital templates, license photos or music.

Active vs Passive Income

- Active: Earned, Profit (requires time and effort).

- Passive: Interest, Rental, Capital Gains, Dividend, Royalty (earn money even when you sleep).

The ultimate goal is shifting from active to passive so you can achieve financial freedom.

Bringing It All Together

Budgeting teaches you discipline, savings give you stability, and multiple income streams give you freedom.

Even if you’re on a low income right now, here’s the roadmap:

- Budget wisely → control your money.

- Save consistently → build your safety net.

- Grow your income → start with earned, then expand into profit and passive streams.

Wealth isn’t built overnight. It’s built paycheck by paycheck, income stream by income stream.

The question to ask yourself is: What’s the one small financial step I can take today? Maybe it’s tracking your expenses. Maybe it’s opening a savings account. Maybe it’s brainstorming a side hustle.

Start small. Stay consistent. Over time, your money will grow—and so will your freedom.