Money has two sides: how you earn it and how you manage it. Most people only focus on the first part — they work hard for a paycheck, hoping it will be enough. But the truth is, relying on just one income stream (usually earned income from a job) can keep you stuck in a cycle where you’re always working, always paying bills, and never really building wealth.

At the same time, debt quietly steals your future. Credit cards, student loans, car payments — they don’t just drain your wallet; they drain your energy, your confidence, and your freedom.

Here’s the good news: you don’t have to stay stuck. By learning about the 7 different types of income and applying the debt snowball strategy to wipe out debt quickly, you can flip your financial script. Instead of your money controlling you, you’ll start controlling it.

This article will guide you step by step:

- First, we’ll break down the 7 types of income and why diversifying them matters.

- Then we’ll dive into the snowball method — a proven way to pay off debt faster.

- Finally, we’ll connect the dots: how eliminating debt gives you the power to grow multiple income streams and build long-term wealth.

Let’s begin with the building blocks of wealth: the seven types of income.

Part 1: The Seven Types of Income Explained

1. Earned Income – Trading Time for Money

This is the most familiar type of income. Earned income comes from your job — whether that’s a salary, hourly wage, or freelance work.

Examples:

- A nurse earning $70,000 per year.

- A retail worker making $15/hour.

- A freelance designer charging clients for projects.

Pros:

- Reliable and straightforward.

- Often includes benefits like healthcare or retirement contributions.

Cons:

- Limited by your time and energy.

- Taxed at the highest rate in most countries.

- Stops when you stop working.

Earned income is where most people start, but it should never be the only stream. It’s the foundation, not the final destination.

2. Profit Income – Owning a Business or Selling Products

Profit income comes from creating or selling something for more than it costs you to make or deliver. Unlike earned income, it’s not limited by your hours — your business or product can work even when you’re asleep.

Examples:

- Running an online store and selling physical or digital products.

- Starting a side hustle like tutoring or consulting.

- Buying something wholesale and selling it at retail price.

Why It Matters: Profit income allows you to scale. A single person working 40 hours a week can only earn so much. But if you own a business, hire others, or create systems, your profit can grow far beyond your personal hours.

3. Interest Income – Making Money While You Sleep

Interest income is earned by lending money to others. Traditionally, this might mean a savings account or government bond. Today, it can also mean peer-to-peer lending or investing in debt securities.

Examples:

- Earning 3% interest from a savings account.

- Buying government bonds.

- Lending money on platforms that connect investors with borrowers.

Why It’s Powerful: Interest income shows how money itself can become a worker. Instead of trading time for money, you’re lending money and getting paid for it.

4. Rental Income – Cash Flow from Property

Rental income is money you earn from renting out real estate you own. This could be residential, commercial, or even short-term rentals like Airbnb.

Examples:

- Owning a duplex and renting out one unit.

- Buying a small office building and leasing it to businesses.

- Renting out a vacation home during peak season.

Pros:

- Steady, predictable cash flow.

- Real estate often appreciates over time, adding capital gains.

Cons:

- Requires upfront capital or financing.

- Can involve maintenance headaches or tenant management.

Still, rental income is one of the most popular wealth-building tools because it combines monthly cash flow with long-term asset growth.

5. Capital Gains – Profiting from Appreciation

Capital gains are profits you make when you sell an asset for more than you bought it. Unlike dividends or rent, capital gains usually come as a lump sum when you sell.

Examples:

- Buying stock at $50 and selling it later at $100.

- Flipping a house for a profit.

- Selling collectibles, like art or rare coins, for more than you paid.

Capital gains can be short-term (assets sold within a year) or long-term (assets held longer), and they’re taxed differently in most countries.

Why It Matters: It rewards smart investing and patience. Buying quality assets and holding them can grow your wealth dramatically over time.

6. Dividend Income – Your Share of Profits

Some companies reward shareholders with dividend payments. This means you don’t have to sell your stocks to make money — you’re literally getting a share of the profits just for owning.

Examples:

- Owning shares of a company like Coca-Cola or Johnson & Johnson that pay regular dividends.

- Investing in dividend-focused ETFs.

Why It’s Powerful: If reinvested, dividends can grow exponentially through compounding. Many people build “dividend portfolios” to eventually replace their job income.

7. Royalty Income – Getting Paid for Creativity and Ownership

Royalty income is money you earn from intellectual property that you own but allow others to use.

Examples:

- A musician earning royalties every time their song is streamed.

- An author getting paid each time a book is sold.

- A software developer licensing their app to businesses.

Why It’s Unique: Royalties are often considered “dream income” because they can keep flowing for years from work you did once.

Quick Recap: The Wealthy’s Secret

The wealthy don’t rely only on earned income. They build multiple streams: profits, dividends, rental income, royalties, and more. That’s why even if one stream slows down, their financial stability remains strong.

Part 2: Why Multiple Income Streams Matter

Let’s pause for a moment. Why not just stick with a paycheck? Because relying on one income stream is risky.

- Lose your job → lose 100% of your income.

- Unexpected expenses → paycheck isn’t enough.

- Inflation → your salary doesn’t stretch as far.

Wealthy people think differently: they build multiple income streams, so they’re never dependent on just one source. Imagine you have:

- Earned income from your job.

- Dividend income from stocks.

- Rental income from a small property.

Even if you lose your job, money is still flowing in. That’s financial security.

Multiple streams don’t just protect you — they accelerate your journey toward financial freedom. Every extra dollar from dividends or side hustles can be invested, snowballing into bigger and bigger wealth.

Part 3: How to Quickly Pay Off Debt – The Snowball Strategy

Now let’s switch gears. Before you can fully enjoy multiple income streams, you need to handle the enemy of wealth: debt.

Debt feels heavy because it steals from your future. But there’s a clear, simple method to destroy it: the debt snowball strategy.

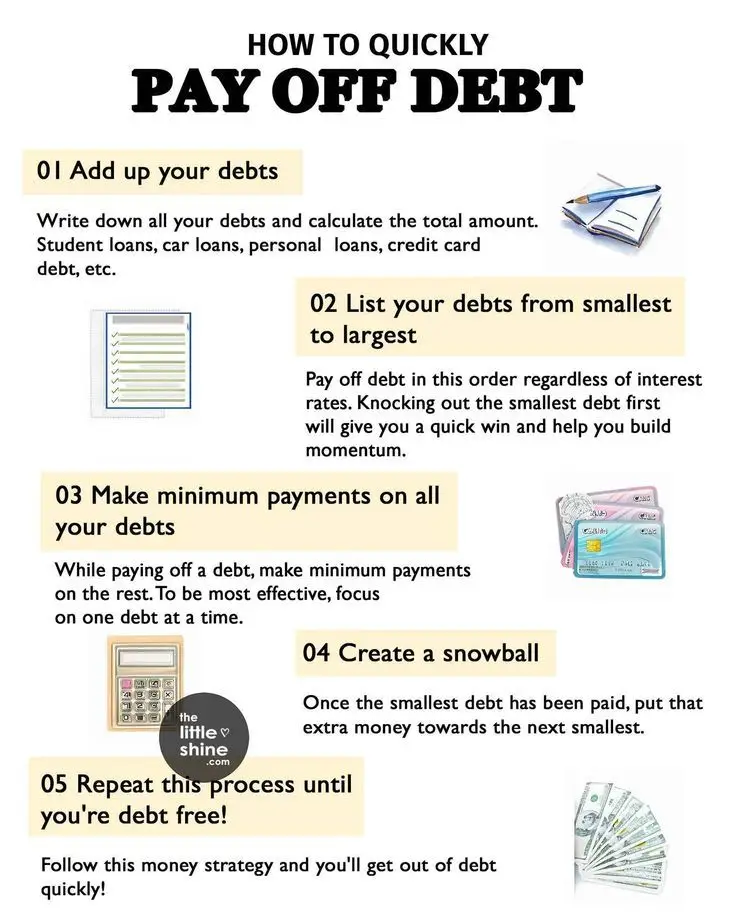

Step 1: Add Up Your Debts

Write them all down. Credit cards, car loans, student loans, personal loans. Seeing the full picture is painful — but it’s the first step to freedom.

Step 2: List Debts from Smallest to Largest

Ignore the interest rates for now. Just order them by balance. Why? Because the smallest debts are the quickest wins. Paying one off gives you momentum and motivation.

Step 3: Make Minimum Payments on All Debts

Stay current on everything to avoid late fees and damage to your credit.

Step 4: Create a Snowball

Put all your extra money toward the smallest debt until it’s gone. Then roll that freed-up payment into the next debt.

Step 5: Repeat Until Debt-Free

With each debt knocked out, your snowball grows. The momentum builds until, suddenly, you’re debt-free.

Why It Works: It’s not about math — it’s about psychology. Quick wins fuel motivation. Motivation keeps you going. And going keeps the snowball rolling.

Part 4: Debt Freedom as the Foundation of Wealth

Once you’re debt-free, your money is no longer trapped in payments. Suddenly, hundreds or even thousands of dollars each month are yours to redirect into savings, investments, or new income streams.

Debt freedom also gives you emotional confidence. Instead of dread when bills arrive, you’ll feel light, in control, and ready to grow.

Part 5: Combining Income Growth with Debt Payoff

Here’s where the two worlds meet.

- Use your extra income streams (like a side hustle, dividends, or freelance gigs) to supercharge your debt snowball.

- Once you’re debt-free, roll that snowball into investments.

- Build streams of income that keep paying you, even when you’re not working.

Example:

- Sarah makes $50,000/year.

- She starts a side hustle making $300/month.

- Instead of spending it, she puts it into her debt snowball.

- She pays off her car loan a year early.

- Now that $400/month car payment is gone — and she invests it instead.

- Fast-forward: that money grows into rental income + dividend income.

This is how ordinary people build extraordinary wealth.

Conclusion: From Surviving to Thriving

Money doesn’t have to be complicated. Start by understanding the 7 types of income. Stop relying only on your paycheck. Explore other streams, even in small ways.

At the same time, free yourself from the chains of debt using the snowball strategy. Every dollar you free becomes a soldier in your army of wealth-building.

This isn’t about overnight success. It’s about steady, consistent progress. One debt at a time. One income stream at a time.

The formula is simple:

Debt freedom + multiple income streams = financial independence.

Start today. Add up your debts. Write down your income streams. Take one small step, and let momentum do the rest.