Managing money isn’t about being perfect. It’s about being intentional.

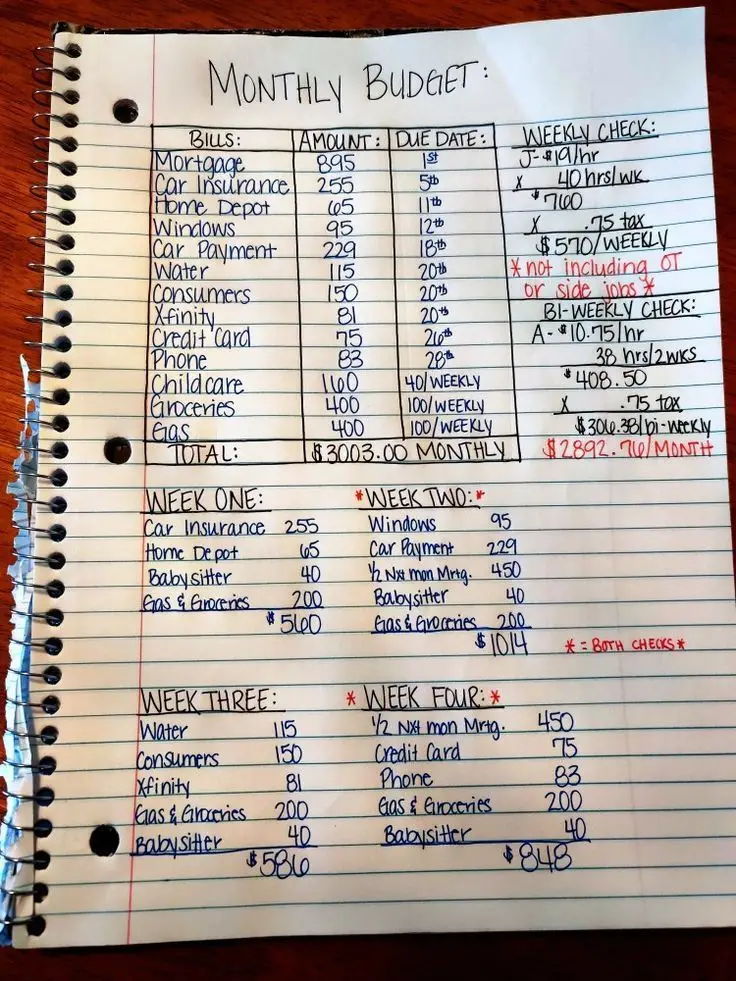

The handwritten “Monthly Budget” sheet shown above is a powerful example of real-world budgeting. It’s simple, direct, and incredibly practical. No fancy apps. No complex spreadsheets. Just clear math, structured planning, and disciplined thinking.

In this article, we’ll break down this monthly budget in detail — how it works, why it works, and how you can apply the same system to your own financial life.

This is more than numbers on paper. This is financial control.

1. The Structure of the Budget

The sheet is divided into four main sections:

- Bills with amounts and due dates

- Income calculation (weekly and bi-weekly)

- Total monthly expenses

- Weekly payment breakdown

This layout is brilliant because it answers the four biggest financial questions:

- How much do I owe?

- When is it due?

- How much do I actually earn?

- How do I distribute payments weekly so I never fall behind?

Most people only track #1.

This budget tracks all four.

2. The Monthly Bills Breakdown

Let’s look at the listed bills and what they represent.

Fixed Monthly Bills

- Mortgage – $895

- Car Insurance – $255

- Home Depot – $65

- Windows – $95

- Car Payment – $229

- Water – $115

- Consumers – $150

- Xfinity – $81

- Credit Card – $75

- Phone – $83

These are recurring obligations. Some are essential (mortgage, utilities), while others may represent installment payments (windows, car payment).

The power here is clarity. Nothing is hidden. Every obligation is visible.

Variable/Weekly-Based Expenses

- Childcare – $160 (40 weekly)

- Groceries – $400 (100 weekly)

- Gas – $400 (100 weekly)

These are flexible but predictable categories.

Instead of pretending they’re “random,” they’re structured into weekly limits.

That is a key discipline move.

3. The Monthly Total: $3,003

The total monthly expense comes to:

$3,003.00

This number is critical.

Why?

Because most people think they know their expenses — but they don’t calculate them precisely.

Once you see the real number, you can make intelligent decisions:

- Is my income covering this?

- Where can I cut?

- What’s my margin?

- Do I need to increase income?

Budgeting begins with truth.

4. Income Breakdown: Weekly & Bi-Weekly Reality Check

This sheet doesn’t just list bills. It calculates income carefully.

Weekly Check

- $9/hour

- 40 hours/week

- $360 gross

- × 0.75 after tax

- = $270/week (approximately shown as $570 weekly including additional income)

There’s also a note:

“Not including OT or side jobs”

That’s smart.

Overtime and side income should never be relied on to survive. They should be extra.

Bi-Weekly Check

- $10.75/hour

- 38 hours/2 weeks

- $408.50

- × 0.75 after tax

- $306.38 bi-weekly

- $2,892.76/month

This gives a realistic after-tax monthly income estimate.

The key lesson:

Budget based on take-home pay — not gross pay.

That one mistake ruins many financial plans.

5. The Most Powerful Part: Weekly Distribution Strategy

This is where this budget becomes advanced.

Instead of waiting for due dates and reacting emotionally, the bills are distributed across four weeks.

This prevents “bill shock.”

Let’s analyze each week.

Week One – $560

- Car Insurance – $255

- Home Depot – $65

- Babysitter – $40

- Gas & Groceries – $200

Total: $560

Week one handles early-month obligations and living expenses.

Notice:

Groceries and gas are pre-limited to $200 weekly.

That creates spending control.

Week Two – $1,014

- Windows – $95

- Car Payment – $229

- Half of next month’s mortgage – $450

- Babysitter – $40

- Gas & Groceries – $200

Total: $1,014

This is a heavy week.

But here’s the genius:

Half of next month’s mortgage is prepaid.

This reduces end-of-month stress.

Pre-paying large bills smooths cash flow.

Week Three – $586

- Water – $115

- Consumers – $150

- Xfinity – $81

- Gas & Groceries – $200

- Babysitter – $40

Total: $586

Mid-month utilities handled cleanly.

No scrambling.

Week Four – $848

- Half of next month’s mortgage – $450

- Credit Card – $75

- Phone – $83

- Gas & Groceries – $200

- Babysitter – $40

Total: $848

Mortgage fully covered for next month.

This creates a psychological buffer.

That buffer is powerful.

6. Why Splitting the Mortgage Is Smart

Instead of paying $895 at once, the budget splits it:

$450 in week two

$450 in week four

This does three important things:

- Prevents cash flow crunch

- Keeps mortgage always one step ahead

- Reduces stress at the beginning of the month

Many financially disciplined families use this exact strategy.

It builds security.

7. Cash Flow vs. Monthly Math

The biggest budgeting mistake is thinking monthly instead of weekly.

Monthly math says:

$3,003 needed.

But weekly planning says:

How do I survive each week comfortably?

Weekly budgeting aligns with how people get paid.

It’s more realistic.

It’s behavioral finance.

8. What This Budget Does Well

Let’s highlight strengths:

✔ Clear total expenses

✔ Includes due dates

✔ Accounts for taxes

✔ Breaks income realistically

✔ Splits large bills

✔ Sets weekly grocery/gas caps

✔ Plans ahead for next month

✔ Doesn’t rely on overtime

This is practical budgeting — not theoretical.

9. Where It Could Be Improved

Even good systems can improve.

Here’s what’s missing:

1. Emergency Fund Allocation

There is no line item for savings.

That’s dangerous.

Even $50/week toward emergency savings would change long-term stability.

2. Retirement Contribution

No visible retirement planning.

Long-term financial security requires investing.

3. Sinking Funds

Categories like:

- Car maintenance

- Medical

- School expenses

- Gifts

- Home repairs

These aren’t listed.

When they show up, they feel like “emergencies.”

But they’re predictable.

10. The Psychological Strength of Writing It Down

There’s something powerful about handwriting a budget.

Research shows that writing by hand increases commitment and retention.

Apps are convenient.

But pen and paper creates accountability.

This sheet shows intentionality.

It reflects someone taking control.

11. The Income Gap Problem

Monthly expenses: $3,003

Monthly income: $2,892.76

There’s a shortfall.

Roughly: $110 deficit.

This means one of three things must happen:

- Increase income

- Reduce expenses

- Use overtime strategically

The note says overtime and side jobs are excluded.

That suggests flexibility.

But ideally, the base income should cover base expenses.

12. Expense Optimization Ideas

If this were your budget, here’s where you might evaluate:

- Can car insurance be reduced?

- Can groceries drop from $400 to $350?

- Can gas be optimized?

- Can credit card payment increase to eliminate debt faster?

Small reductions compound.

Even $150 saved monthly equals $1,800 yearly.

13. The Discipline of Weekly Grocery Caps

$100/week groceries.

This forces planning:

- Meal prep

- Shopping lists

- Avoiding impulse buys

- Using discounts

Budgeting groceries weekly instead of monthly prevents overspending early.

It creates rhythm.

14. Why This System Prevents Late Fees

Bills are paid before due dates.

That eliminates:

- Late fees

- Credit score damage

- Stress calls

- Overdraft fees

Financial organization reduces emotional burden.

15. How to Build Your Own Version

Step 1: List every bill

Step 2: Write exact amounts

Step 3: Include due dates

Step 4: Calculate after-tax income

Step 5: Break into weekly chunks

Step 6: Pre-plan heavy weeks

Step 7: Add savings line

Step 8: Review monthly

That’s it.

Simple but powerful.

16. The Real Purpose of Budgeting

Budgeting isn’t about restriction.

It’s about direction.

This sheet shows someone directing their money instead of reacting to it.

Every dollar has a job.

That’s financial maturity.

17. What This Budget Represents

Beyond math, this budget represents:

- Responsibility

- Planning

- Family stability

- Financial awareness

- Effort to improve

It’s easy to criticize numbers.

It’s harder to respect discipline.

This sheet deserves respect.

18. The Long-Term Growth Strategy

If this person:

- Eliminates credit card debt

- Reduces insurance costs

- Builds emergency savings

- Increases income through skill growth

Within 2–3 years, this could transform into:

- Strong savings buffer

- Mortgage acceleration

- Investment contributions

- Financial peace

Budgeting is step one.

Wealth building is step two.

19. The Most Important Takeaway

The biggest lesson from this budget is not math.

It’s control.

When you know:

- What you earn

- What you owe

- When it’s due

- How it’s distributed

Money stops being chaotic.

It becomes structured.

Structure creates confidence.

20. Final Thoughts

This simple handwritten monthly budget demonstrates financial awareness many people never develop.

It shows:

- Planning

- Intentional living

- Income tracking

- Expense discipline

- Weekly structure

Is it perfect?

No.

Is it effective?

Absolutely.

The real power isn’t in the numbers.

It’s in the decision to take ownership.

If you’ve never created a detailed budget like this, now is the time.

Because financial freedom doesn’t begin with more money.

It begins with clarity.

And clarity begins on paper.