Managing money can feel overwhelming. Should you keep more cash in your checking account? Is a savings account enough, or should you invest? What about retirement accounts, health savings accounts, or brokerage funds?

The truth is, financial peace comes from organizing your money into the right accounts. Each account has a specific role—some provide safety and liquidity, while others focus on long-term growth and tax advantages.

In this guide, we’ll break down exactly how much money to keep in each account, why it matters, and how to build your financial system step by step.

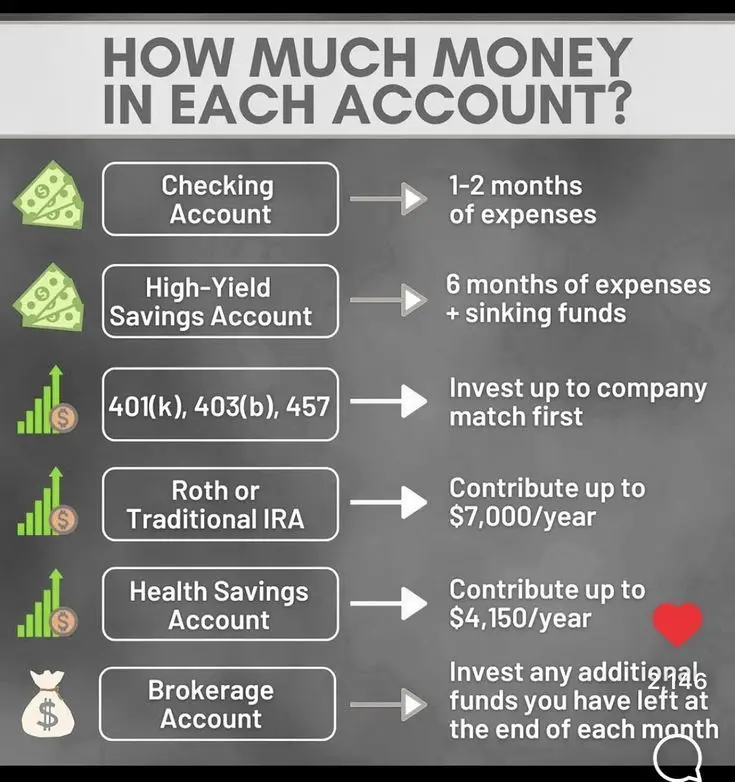

1. Checking Account → 1–2 Months of Expenses

Your checking account is your financial hub. It’s where your paycheck lands, and it’s the account you use to pay bills, swipe your debit card, or withdraw cash.

But here’s the key: your checking account is not meant to hold all your money.

Why only 1–2 months of expenses?

- Checking accounts typically earn little to no interest. Keeping too much here means your money isn’t growing.

- The main purpose is easy access for recurring expenses like rent, utilities, groceries, and subscriptions.

- By capping the balance, you prevent overspending since excess funds are moved elsewhere (like savings or investments).

Example:

If your monthly expenses are $2,500, aim to keep $2,500–$5,000 in checking at all times.

Anything above that? Sweep it into savings or investments.

2. High-Yield Savings Account → 6 Months of Expenses + Sinking Funds

A High-Yield Savings Account (HYSA) is your safety net. It’s federally insured, earns more interest than checking, and is perfect for your emergency fund.

Why 6 months of expenses?

- Financial experts recommend 3–6 months of expenses, but 6 months is safer.

- This protects you in case of job loss, medical emergencies, or unexpected repairs.

Sinking funds are another reason to use HYSA. These are mini savings accounts for planned, irregular expenses like:

- Car repairs

- Annual insurance premiums

- Holiday gifts

- Travel

By storing these in a HYSA, you separate them from your “spending money” while still earning interest.

Example:

- Monthly expenses: $2,500

- Emergency fund goal: $15,000

- Add sinking funds: $2,000 (car, vacation, etc.)

- Total HYSA target = $17,000

3. 401(k), 403(b), 457 → Invest Up to Company Match First

Workplace retirement accounts (like 401(k), 403(b), or 457 plans) are often the best starting point for long-term investing—especially if your employer offers a match.

What’s a match?

- Many employers contribute extra money when you contribute to your retirement plan.

- Example: If your employer matches 100% of your contribution up to 5% of your salary, and you earn $60,000, then contributing $3,000 gets you an extra $3,000 free money.

Why prioritize the match first?

- It’s literally a 100% return on investment.

- Skipping the match = leaving free money on the table.

Contribution limits (2024):

- $23,000/year for individuals under 50.

- $30,500/year for age 50+ (catch-up).

Start with the match, then move on to IRAs or HSAs before maxing out the full 401(k).

4. Roth or Traditional IRA → Contribute Up to $7,000/year

IRAs (Individual Retirement Accounts) are powerful tools that give you tax advantages outside your workplace plan.

Roth IRA

- Contributions are made with after-tax money.

- Growth is tax-free.

- Withdrawals in retirement are also tax-free.

- Great if you expect to be in a higher tax bracket later.

Traditional IRA

- Contributions may be tax-deductible now.

- Growth is tax-deferred.

- Withdrawals in retirement are taxed.

- Great if you expect to be in a lower tax bracket later.

Contribution limit (2024):

- $7,000/year (under age 50).

- $8,000/year (age 50+ with catch-up).

Strategy:

- If your employer offers a match → contribute enough to get it.

- Then max out your Roth IRA (if eligible).

- After that, return to your 401(k) to contribute more if possible.

5. Health Savings Account (HSA) → Contribute Up to $4,150/year

An HSA is the triple tax advantage unicorn of personal finance. It’s only available if you have a high-deductible health plan (HDHP), but if you qualify, it’s one of the most powerful accounts out there.

Benefits of HSA:

- Contributions are tax-deductible.

- Growth is tax-free.

- Withdrawals for qualified medical expenses are tax-free.

Even better, after age 65, you can use HSA funds for anything (not just medical) — withdrawals are then treated like a Traditional IRA.

Contribution limit (2024):

- $4,150/year for individuals.

- $8,300/year for families.

- Extra $1,000 if age 55+.

Pro tip:

- Many people use HSAs as a stealth retirement account by paying medical expenses out of pocket now, letting the HSA grow untouched for decades.

6. Brokerage Account → Invest Any Extra

Once you’ve filled your safety net, maxed out retirement accounts, and contributed to your HSA, any additional money can go into a taxable brokerage account.

Why use a brokerage account?

- Total flexibility → no contribution limits.

- No penalties for early withdrawals.

- Perfect for medium-term goals (5–15 years) like buying a house, starting a business, or building wealth beyond retirement.

Downside:

- No tax breaks like retirement accounts.

- You’ll pay capital gains taxes when selling investments.

But the trade-off is worth it if you’ve already taken care of the tax-advantaged accounts.

7. Putting It All Together – Order of Operations

Here’s the recommended flow of money each month:

- Checking account → cover 1–2 months of expenses.

- High-Yield Savings Account → build emergency fund + sinking funds.

- Workplace retirement plan (401k, 403b, 457) → contribute enough to get the employer match.

- IRA (Roth or Traditional) → max out contributions ($7,000).

- HSA → contribute up to the annual limit ($4,150 individual).

- Back to 401(k) → add more if you can, up to annual max.

- Brokerage account → invest leftover funds for long-term goals.

This order balances safety, tax advantages, and growth.

8. Example Walkthrough

Let’s say you make $70,000 a year. Here’s how your system might look:

- Checking: $5,000 (2 months of expenses).

- HYSA: $18,000 (6 months + sinking funds).

- 401(k): Contribute 5% ($3,500) to get full employer match ($3,500).

- Roth IRA: Contribute $7,000.

- HSA: Contribute $4,150.

- Extra left at end of year: Invest in brokerage.

By the end of the year, you’ve covered emergencies, captured free employer money, maxed out tax-advantaged accounts, and invested extra—all while still having cash flow in checking.

Conclusion

Financial peace comes not just from how much you earn, but from how you organize what you have. Each account plays a role:

- Checking for bills.

- Savings for emergencies.

- Retirement accounts for future wealth.

- HSAs for health and stealth savings.

- Brokerage accounts for freedom and growth.

When you distribute your money strategically across these buckets, you create a financial system that protects you now, supports you later, and grows your wealth in the background.

So ask yourself: do you have money sitting idle in the wrong place? If so, it’s time to move it into the right account—and give every dollar a job.