Money isn’t just a tool—it’s a roadmap. And like any good roadmap, it works best when you know your destination and plot the journey in stages. Your financial priorities naturally evolve as you age, and what matters in your 20s is vastly different from your 50s or 60s.

Breaking your financial life down by decade gives you clarity and focus. It helps you set realistic goals, avoid common pitfalls, and build momentum. Think of it as climbing a mountain: each decade is a base camp. Miss one, and the summit—financial independence and retirement security—becomes harder to reach.

The earlier you start, the more you benefit from compound growth, smarter decision-making, and financial resilience. Even if you’re starting late, knowing the “decade roadmap” gives you a structured path forward.

In this guide, we’ll walk through each decade of your life, detailing what you should focus on, what financial milestones to hit, and how to build habits that stick.

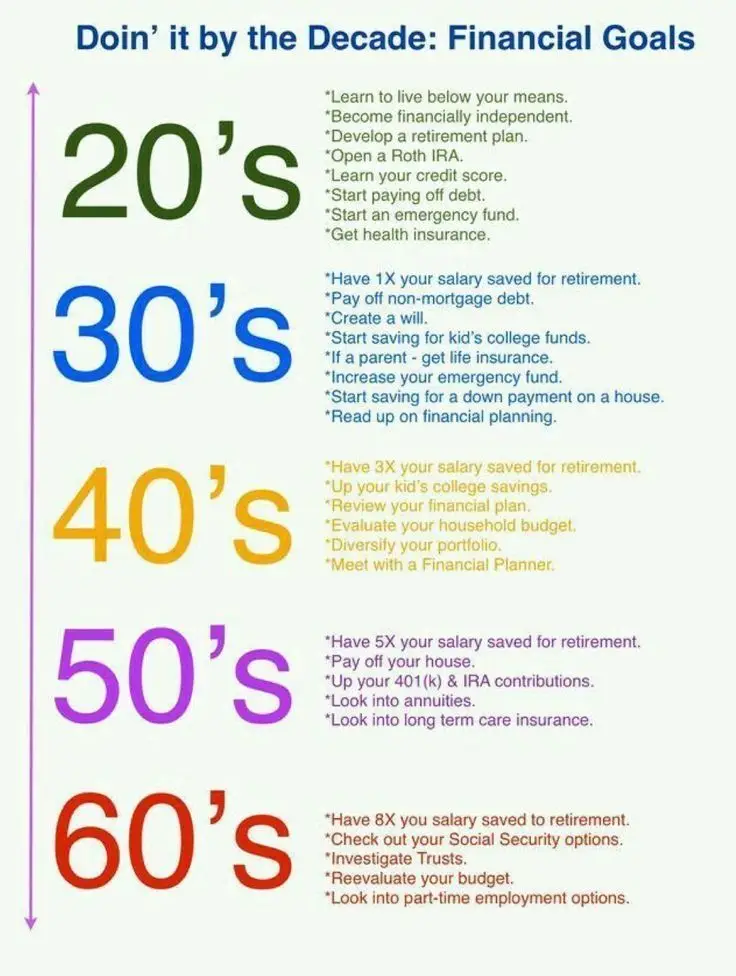

Your 20s: Laying the Foundation

Your 20s are arguably the most critical decade for financial habits. The choices you make now compound over decades, shaping the trajectory of your wealth. It’s not about making millions immediately—it’s about building strong financial habits, avoiding debt traps, and starting early on retirement savings.

1. Learn to Live Below Your Means

This is the golden rule of personal finance: spend less than you earn. Sounds simple, but lifestyle inflation makes it tricky. As your income rises, so do your expenses—new gadgets, fancy dinners, and trend-driven purchases.

- Tip: Track every expense for a month. Identify “wants” vs. “needs.”

- Example: If you earn $3,000 a month, aim to live on $2,500. Save or invest the rest.

- Mindset: Your 20s are the decade to delay gratification. That latte or the latest gadget might feel essential now, but the long-term payoff of financial discipline is far sweeter.

2. Become Financially Independent

Financial independence means having control over your money rather than letting it control you. It doesn’t mean being rich—it means covering your expenses without stress and having options.

- Start small: Automate savings, reduce unnecessary spending, and understand your cash flow.

- Goal: Being able to cover 3–6 months of expenses without relying on anyone.

3. Develop a Retirement Plan

It might feel like retirement is light-years away, but your 20s are prime time to start saving. Time is your ally: the earlier you invest, the more compound interest works in your favor.

- Actionable step: Open a retirement account, even if you can only contribute $50/month.

- Rationale: A $50/month investment at 7% annual growth over 40 years becomes nearly $250,000. Small steps add up.

4. Open a Roth IRA

A Roth IRA is a retirement account that allows tax-free growth and tax-free withdrawals in retirement. For young earners in lower tax brackets, it’s ideal.

- Tip: Contribute as much as you can early. Even a few hundred dollars per month makes a big difference.

- Bonus: The Roth IRA gives you flexibility—you can withdraw contributions (not earnings) without penalty, which is handy in emergencies.

5. Learn Your Credit Score

Your credit score affects everything: renting an apartment, buying a car, qualifying for a mortgage, even some jobs.

- Actionable step: Get a free credit report from annualcreditreport.com.

- Tip: Pay bills on time, keep credit utilization below 30%, and avoid opening unnecessary credit accounts.

6. Start Paying Off Debt

Debt in your 20s can snowball into decades of financial stress. Start with high-interest debt like credit cards.

- Strategy: Use the debt avalanche method (pay off highest interest first) or debt snowball (pay off smallest balances first for motivation).

- Goal: Aim to be debt-free (excluding student loans or mortgage) by your 30s.

7. Start an Emergency Fund

Life is unpredictable. An emergency fund acts as a financial safety net.

- Recommendation: Save 3–6 months of living expenses.

- Tip: Keep it in a high-yield savings account for easy access.

- Example: If monthly expenses are $2,000, target $6,000–$12,000.

8. Get Health Insurance

Medical emergencies can destroy finances if you’re uninsured. Health insurance protects both your wallet and your well-being.

- Tip: Compare plans carefully. Consider premiums, deductibles, and coverage.

- Extra advice: Don’t skip preventive care—it keeps costs down in the long run.

Key Takeaways for Your 20s

- Discipline now = freedom later. Every dollar saved or invested compounds over time.

- Debt is a tool, not a lifestyle. Use it wisely.

- Financial education pays the best interest. Learn about investing, taxes, insurance, and retirement now.

- Start small, stay consistent. Even tiny actions today can snowball into life-changing outcomes decades later.

Your 30s: Building Stability

Your 30s are all about building on the foundation you set in your 20s. By now, you’ve hopefully learned to live below your means, manage debt, and start saving for the future. In your 30s, life usually gets a little more complex: careers accelerate, families grow, and long-term financial planning becomes essential. This decade is about stability, growth, and smart planning.

1. Have 1X Your Salary Saved for Retirement

By age 30–35, aim to have at least one year’s salary saved for retirement. If you earn $60,000, your retirement savings should be around $60,000.

- Why it matters: The earlier you hit milestones, the more flexibility you have later.

- Tip: Maximize contributions to your 401(k) or Roth IRA if possible.

- Example: Increasing contributions by 1–2% of your income annually can add tens of thousands over decades.

2. Pay Off Non-Mortgage Debt

Your 30s are the time to tackle lingering debts—credit cards, personal loans, and student loans (outside of your mortgage, if you have one).

- Strategies:

- Debt avalanche: Pay off the highest interest first for maximum savings.

- Debt snowball: Pay off smaller balances first for motivation.

- Result: Less stress, more cash flow, and a stronger credit profile.

3. Create a Will

Even if you’re young and healthy, a will protects your assets and ensures your wishes are honored.

- Tip: Include guardianship instructions if you have children.

- Action step: You don’t need a complicated estate—basic wills are inexpensive but crucial.

- Extra: Consider powers of attorney and healthcare directives for full protection.

4. Start Saving for Your Children’s College Fund

If you’re a parent or planning to be one, college savings should enter your financial plan. Education costs rise faster than inflation, so early action matters.

- Options: 529 plans, custodial accounts, or Roth IRAs (for parents who want flexibility).

- Tip: Even small monthly contributions can grow substantially over 15–18 years.

5. If a Parent – Get Life Insurance

Life insurance becomes essential if others rely on your income.

- Term life insurance: Affordable and sufficient for most young families.

- Rule of thumb: Coverage should be 10–15 times your annual income.

- Purpose: Protects dependents, pays off debts, and secures children’s education funds.

6. Increase Your Emergency Fund

Life in your 30s often comes with bigger expenses: mortgage, kids, car payments. Your emergency fund should grow to cover 6–12 months of expenses.

- Tip: Keep it in a high-yield savings account or money market fund for easy access.

- Example: If monthly expenses are $4,000, target $24,000–$48,000 in your fund.

7. Start Saving for a Down Payment on a House

Homeownership is a common goal in your 30s, and preparing early is key.

- Target: 20% down payment to avoid private mortgage insurance (PMI).

- Strategy: Open a dedicated savings account, automate contributions, and research housing markets.

- Tip: Don’t sacrifice emergency funds for a down payment—balance is critical.

8. Read Up on Financial Planning

Your 30s are a great time to educate yourself about money. Understanding investing, taxes, retirement accounts, and estate planning gives you control over your financial future.

- Recommended reads:

- Personal finance books like The Simple Path to Wealth or Your Money or Your Life

- Blogs, podcasts, and reputable financial news sites

- Why: Knowledge reduces costly mistakes and empowers confident decisions.

Key Takeaways for Your 30s

- Stability is the goal: Reduce debt, increase savings, and protect your family.

- Retirement planning continues: One year of salary saved by now sets you up for compounding success.

- Family-focused financial planning: Life insurance, wills, and college savings become priorities.

- Education and foresight pay off: Understanding your finances now saves stress later.

Your 40s: Expanding & Diversifying

Your 40s are often the busiest financial decade. By now, your career is likely more established, your kids are growing, and your financial obligations are at their peak. This is the time to review, adjust, and diversify your finances—making sure your earlier efforts are compounding toward long-term security.

1. Have 3X Your Salary Saved for Retirement

By your 40s, you should aim for three times your annual salary saved for retirement.

- Example: If you earn $80,000/year, your retirement accounts should hold around $240,000.

- Why: You’re getting closer to the point where catch-up contributions matter. The earlier you hit these milestones, the more flexibility you’ll have in your 50s and 60s.

- Actionable tip: Increase your retirement contributions annually, ideally with automatic payroll deductions.

2. Up Your Kids’ College Savings

College costs continue to rise, so it’s time to accelerate contributions if you haven’t maxed them yet.

- Strategy: Reassess your 529 plan contributions or consider additional investment accounts if needed.

- Tip: Encourage older kids to apply for scholarships and financial aid—every little bit helps.

- Example: A 15-year-old with a $20,000 college fund may need an additional $5,000–$10,000 contribution to keep up with tuition inflation.

3. Review Your Financial Plan

Life changes quickly, and your financial plan should reflect reality.

- Steps:

- Reassess retirement goals based on current savings and projected expenses.

- Adjust insurance coverage if your family or career changes.

- Factor in upcoming milestones, like paying off a mortgage or college tuition.

- Tip: A detailed review every 1–2 years helps avoid surprises later.

4. Evaluate Your Household Budget

Your 40s often bring higher expenses: mortgage, kids’ activities, healthcare, and lifestyle inflation.

- Actionable tips:

- Track your monthly spending to identify areas to cut or optimize.

- Automate savings and bill payments to reduce stress.

- Reassess discretionary spending—vacations, dining out, subscriptions.

- Mindset: Focus on efficiency, not deprivation. Smart budgeting allows you to save more without sacrificing quality of life.

5. Diversify Your Portfolio

Investments matter now more than ever. Diversification reduces risk and ensures your portfolio can weather market volatility.

- Principle: Don’t put all your eggs in one basket. Mix stocks, bonds, real estate, and other assets.

- Tip: Consider dollar-cost averaging—investing a fixed amount regularly—to reduce timing risk.

- Action: Review allocation annually and rebalance if needed to stay on track for retirement.

6. Meet With a Financial Planner

A professional can help you fine-tune your strategy for retirement, college funding, estate planning, and taxes.

- Why: Financial planners bring expertise, help identify blind spots, and can save you money in the long run.

- Tip: Look for fee-only planners with fiduciary responsibility—they work for you, not commissions.

- Alternative: If hiring a planner isn’t feasible, leverage online planning tools or workshops to stay informed.

Key Takeaways for Your 40s

- This is a decade of growth and review: Your finances are more complex, and regular assessment is key.

- Increase savings strategically: Retirement and college contributions should ramp up.

- Optimize your household budget: Efficient spending frees resources for long-term goals.

- Diversify investments: Protect your wealth while still aiming for growth.

- Professional guidance pays off: A planner or advisor can help ensure you stay on track.

Your 50s: Approaching Peak Financial Health

Your 50s are a pivotal decade in financial planning. By now, your earnings may be near their peak, your children may be approaching financial independence, and your focus shifts to retirement readiness, paying off major debts, and safeguarding your health and wealth.

1. Have 5X Your Salary Saved for Retirement

By your 50s, your retirement savings goal should be roughly five times your annual salary.

- Example: If you earn $100,000/year, aim for $500,000 saved.

- Why it matters: This benchmark ensures that you can maintain your lifestyle once you retire and cover unexpected costs without dipping into other assets.

- Actionable tip: Maximize contributions to your 401(k), IRA, or Roth IRA. Take advantage of catch-up contributions if you’re 50 or older—an extra $7,500 for 401(k) and $1,000 for IRA annually (2025 limits).

2. Pay Off Your House

Mortgage freedom dramatically reduces financial stress. If you haven’t already, your 50s are the decade to eliminate housing debt.

- Tip: Prioritize extra payments on the principal. Even small additional payments each month can shorten your mortgage by years and save tens of thousands in interest.

- Mindset: Being mortgage-free gives you flexibility in retirement, reduces monthly expenses, and allows you to redirect funds toward investments or lifestyle goals.

3. Increase Your 401(k) & IRA Contributions

With children potentially becoming financially independent, this is the perfect time to ramp up retirement contributions.

- Strategy:

- Max out regular contributions.

- Add catch-up contributions if eligible.

- Review investment allocations for a balance of growth and risk management.

- Tip: Automate contributions and treat them as untouchable expenses.

4. Look Into Annuities

Annuities are financial products that guarantee a steady income stream during retirement. While not for everyone, they can provide stability for those concerned about outliving their savings.

- Types: Fixed, variable, and indexed annuities.

- Actionable tip: Compare fees, guarantees, and flexibility. Consult a financial planner to see if an annuity complements your retirement portfolio.

5. Look Into Long-Term Care Insurance

As we age, healthcare costs rise—sometimes unexpectedly. Long-term care insurance protects your assets from being drained by prolonged medical or nursing home care.

- Tip: Buy insurance sooner rather than later, as premiums increase with age and pre-existing conditions can make you ineligible.

- Considerations: Evaluate coverage limits, waiting periods, and inflation protection to ensure the policy aligns with your projected needs.

Key Takeaways for Your 50s

- Retirement readiness is the focus: Aim for 5X your salary in savings and maximize contributions.

- Eliminate high-cost debts: Paying off your mortgage creates flexibility and peace of mind.

- Consider guaranteed income options: Annuities can stabilize retirement income.

- Protect against health uncertainties: Long-term care insurance is a safeguard for your family and savings.

- Plan for legacy and lifestyle: With proper preparation, your 50s can be the decade where you gain financial confidence and security.

Your 60s: Retirement Ready

Your 60s mark the transition from earning to enjoying the fruits of decades of disciplined financial planning. By now, your focus shifts from accumulation to preservation, optimization, and legacy planning.

1. Have 8X Your Salary Saved for Retirement

By your 60s, your goal should be roughly eight times your annual salary in retirement savings.

- Example: If your salary is $100,000, your savings goal should be around $800,000.

- Why it matters: This level of savings, combined with Social Security and any pension income, ensures a comfortable lifestyle without the fear of running out of money.

- Tip: Continue contributions to retirement accounts, but also consider reallocating investments toward more conservative, low-risk options to protect your nest egg.

2. Check Out Your Social Security Options

Social Security becomes a critical part of retirement planning. Deciding when and how to claim benefits can have a significant impact on lifetime income.

- Tip: Delaying benefits past the full retirement age increases your monthly payment.

- Strategy: Evaluate your health, retirement savings, and life expectancy to choose the optimal claiming age.

- Extra: Coordinate with your spouse if married to maximize household benefits.

3. Investigate Trusts

Trusts can help manage wealth efficiently, reduce estate taxes, and protect assets for heirs.

- Why: They provide control over how assets are distributed and can safeguard beneficiaries who are minors or financially inexperienced.

- Tip: Work with an estate planning attorney to set up the right type of trust for your situation—revocable, irrevocable, or special purpose.

4. Reevaluate Your Budget

Your lifestyle and expenses often change in retirement. Regularly review and adjust your budget to match your income and spending patterns.

- Tips:

- Track discretionary spending to ensure it aligns with your retirement goals.

- Identify areas where you can downsize or optimize, such as housing, travel, or subscriptions.

- Mindset: Flexibility is key. Life expectancy and unexpected medical costs can affect retirement plans, so your budget should allow room for adjustments.

5. Look Into Part-Time Employment Options

Even in retirement, many people choose part-time work for extra income, social engagement, or personal fulfillment.

- Benefits:

- Supplemental income can reduce withdrawals from retirement savings.

- Keeps you active and engaged socially.

- Offers purpose and structure to your days.

- Examples: Consulting in your career field, freelance work, tutoring, or starting a small passion business.

Key Takeaways for Your 60s

- Preservation is the priority: Protect the nest egg you’ve built over decades.

- Optimize retirement income: Social Security, pensions, and investments must work together efficiently.

- Plan your legacy: Trusts and estate planning protect your wealth and ensure your wishes are honored.

- Adjust your lifestyle: Budget for retirement realities while maintaining quality of life.

- Stay active and purposeful: Part-time work or volunteering provides financial flexibility and personal fulfillment.

Conclusion: Financial Planning is a Lifelong Journey

From your 20s to your 60s, financial planning is a decade-by-decade journey. Each stage builds on the last:

- 20s: Build habits and foundations.

- 30s: Stabilize and protect your growing responsibilities.

- 40s: Expand and diversify your assets.

- 50s: Maximize savings, eliminate debts, and safeguard your health.

- 60s: Preserve wealth, optimize retirement income, and plan your legacy.

No matter where you are in your journey, it’s never too late to start. Consistency, discipline, and education compound over time—more than any single paycheck ever could. The key is starting now, staying informed, and revisiting your plan regularly.

With decade-based goals, you have a roadmap to financial confidence, security, and independence, ensuring that you can enjoy each stage of life on your own terms.