In today’s fast-paced world, managing personal finances can often take a backseat to other pressing priorities. Yet, maintaining financial health is crucial for long-term stability and peace of mind. “Deep Clean Your Finances in 1 Month” is designed to help you transform your financial situation through a structured, step-by-step approach. Whether you’re tackling debt, setting up a budget, or planning for future investments, this guide will provide you with the tools and knowledge to take control of your financial destiny.

Many individuals find themselves overwhelmed by the complexity of financial management. Bills pile up, expenses go untracked, and savings plans fall by the wayside. This guide aims to simplify the process, breaking it down into manageable tasks that can be accomplished over the course of a month. By dedicating just a little time each day, you’ll be able to achieve a comprehensive financial overhaul.

What sets this program apart is its holistic approach. We don’t just focus on cutting costs or increasing savings; we delve into the psychological aspects of spending and saving, helping you understand your financial habits and how to change them. This journey is about more than just numbers; it’s about building a healthier relationship with money.

Technical History

The Evolution of Personal Finance Management

Managing personal finances has come a long way from the days of balancing a checkbook with pen and paper. The technical evolution in personal finance management can be traced back to the introduction of personal computers in the late 20th century. Early software tools, such as Quicken, revolutionized the way individuals could track their finances, offering digital ledgers that simplified budgeting and accounting tasks.

As technology advanced, so did the tools available for financial management. The internet boom of the late 1990s and early 2000s brought about a significant shift, with online banking becoming a standard offering by most financial institutions. This development allowed individuals to monitor their accounts and transactions in real-time, paving the way for more dynamic and interactive financial management solutions.

The Rise of Fintech and Mobile Applications

The past decade has seen an explosion in financial technology (fintech) innovations, particularly with the rise of smartphones and mobile applications. Apps like Mint, YNAB (You Need a Budget), and Personal Capital have made it easier than ever for users to manage their finances on-the-go. These applications offer a wide range of features, from automatic expense tracking to personalized budgeting advice, leveraging data analytics to provide users with insights into their spending habits.

Moreover, fintech has democratized financial services, providing access to tools and resources that were once only available to financial professionals. Investment platforms like Robinhood and Acorns have lowered the barriers to entry for stock market participation, while peer-to-peer payment apps like Venmo and Cash App have simplified the process of transferring money between individuals.

The Impact of Artificial Intelligence and Machine Learning

In recent years, artificial intelligence (AI) and machine learning (ML) have begun to play a significant role in personal finance management. These technologies enable more sophisticated data analysis, allowing financial management tools to offer predictive insights and automated recommendations. For example, AI-powered chatbots can provide instant customer support and financial advice, while ML algorithms can identify patterns in spending behavior and suggest ways to optimize savings.

Robo-advisors, which utilize AI to provide automated investment advice, have also gained popularity. These platforms offer personalized portfolio management at a fraction of the cost of traditional financial advisors, making investment services more accessible to a broader audience.

Security and Privacy Concerns

With the increasing reliance on digital tools for financial management, concerns about security and privacy have become paramount. Financial institutions and fintech companies invest heavily in advanced encryption technologies and secure authentication methods to protect user data. However, users must remain vigilant, practicing good digital hygiene and staying informed about potential threats like phishing scams and data breaches.

The introduction of blockchain technology has also had a significant impact on financial security. By providing a decentralized and immutable ledger system, blockchain offers a new level of transparency and security for financial transactions, although its adoption in personal finance is still in its early stages.

Looking ahead, the future of personal finance management is likely to be shaped by continued advancements in technology and an increasing emphasis on personalized financial wellness. As AI and ML technologies become more sophisticated, we can expect even more tailored financial advice and automation, reducing the time and effort required to manage personal finances.

Furthermore, the integration of financial management tools with other aspects of personal well-being, such as mental health and lifestyle choices, is likely to become more prevalent. This holistic approach recognizes that financial health is deeply interconnected with overall well-being, encouraging individuals to consider their financial decisions in the context of their broader life goals.

In conclusion, the technical history of personal finance management reflects a journey from manual record-keeping to a highly digitized and automated process. As we move forward, embracing the opportunities presented by new technologies will be key to achieving financial stability and success in an ever-changing world.

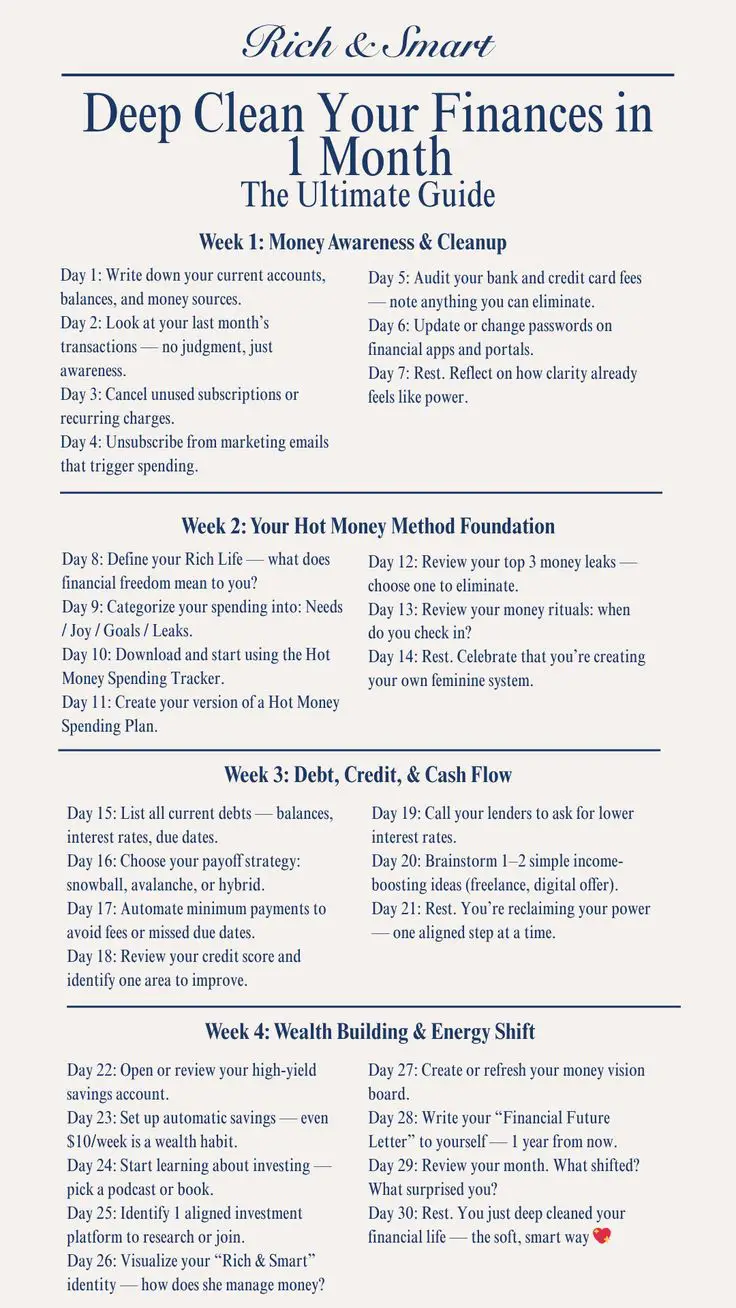

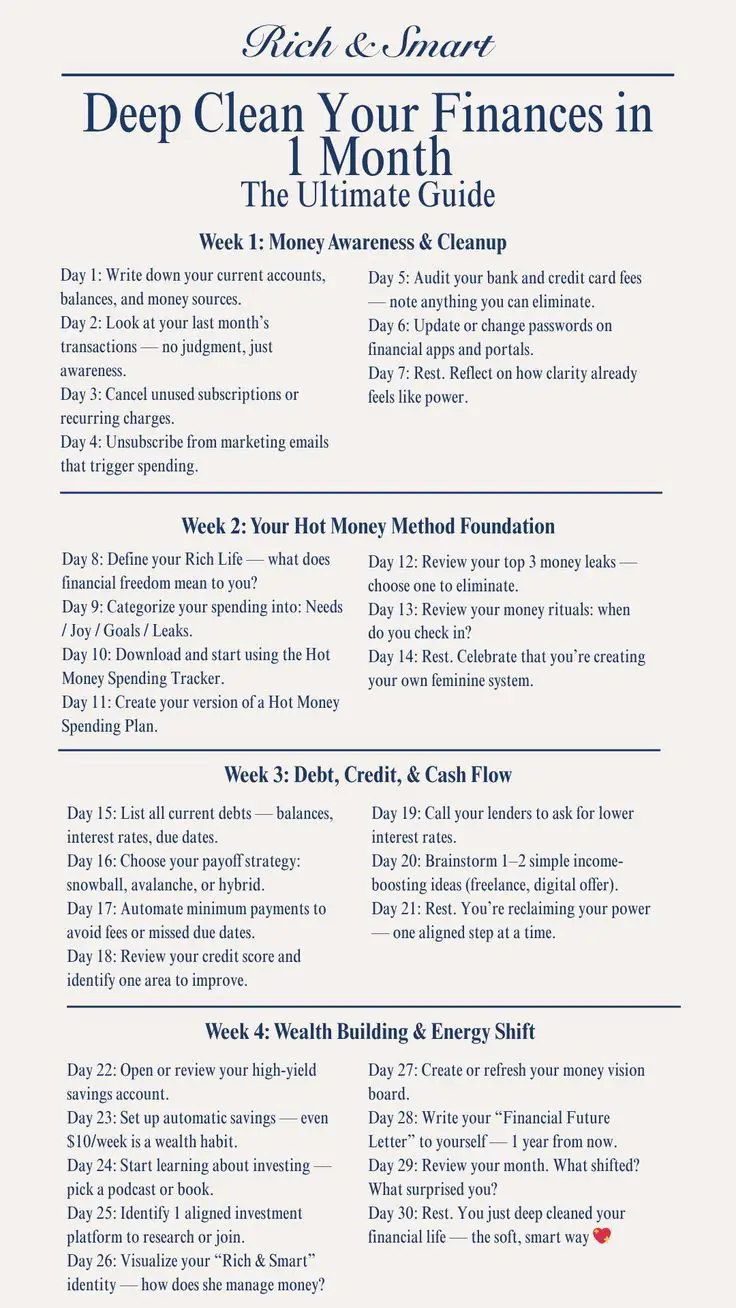

Deep Clean Your Finances in 1 Month

Deep Clean Your Finances in 1 Month: A Practical Guide

Taking control of your finances can seem daunting, but with a structured plan, you can deep clean your financial life in just one month. This guide will walk you through the steps you need to take each week to achieve financial clarity and freedom.

Week 1: Assess and Organize

The first step in deep cleaning your finances is to assess your current situation and organize your financial documents. This week is about gathering information and setting the stage for the changes you’ll make in the coming weeks.

Gather Financial Documents: Collect all bank statements, credit card statements, bills, and any financial documents you have. Organize them in a folder or use digital tools to keep them in one place.

Create a Financial Inventory: List all your assets (savings, investments, property) and liabilities (debts, loans). This will give you a clear picture of your net worth.

Review Your Monthly Spending: Analyze your spending habits by reviewing previous months’ bank and credit card statements. Categorize your expenses to identify areas where you can cut back.

Week 2: Budget and Plan

In the second week, focus on creating a realistic budget and setting financial goals. This will help you manage your money more effectively and work towards achieving your financial ambitions.

Create a Budget: Based on your financial inventory and spending analysis, create a budget that aligns with your income and financial goals. Ensure that your budget includes savings and debt repayment.

Set Financial Goals: Define short-term and long-term financial goals. Whether it’s saving for a vacation, paying off debt, or building an emergency fund, having clear goals will keep you motivated.

Track Your Progress: Use budgeting apps or spreadsheets to track your spending and ensure you’re sticking to your budget. Adjust as necessary to stay on track.

Week 3: Reduce Debt and Boost Savings

With a budget in place, it’s time to tackle debt and increase your savings. This week, focus on strategies to pay down debt and build your savings.

Prioritize Debt Repayment: Focus on paying off high-interest debt first, such as credit cards. Consider using the snowball or avalanche method to systematically reduce your debt.

Increase Your Savings: Allocate a portion of your budget to savings. Set up automatic transfers to a savings account to ensure you’re consistently saving.

Build an Emergency Fund: Aim to save at least three to six months’ worth of living expenses. This fund will provide financial security in case of unexpected events.

Week 4: Optimize and Maintain

The final week is about optimizing your finances and establishing habits that will help you maintain financial health in the long term.

Review Subscriptions and Expenses: Cancel any unnecessary subscriptions or recurring charges. Look for areas where you can reduce expenses without compromising your lifestyle.

Optimize Investments: Review your investment portfolio and make adjustments as needed. Consider speaking with a financial advisor for professional advice.

Plan for the Future: Start thinking about retirement planning and other long-term financial strategies. The earlier you start, the better prepared you’ll be.

1. How do I start organizing my financial documents?

Begin by gathering all physical and digital financial documents. Use folders or a digital tool to categorize them into sections such as bills, banking, and investments. This will make it easier to access and manage them.

2. What is the most effective way to create a budget?

Start by analyzing your income and expenses. Use this information to create a realistic budget that includes savings and debt repayment. Consider using budgeting apps for easier tracking and adjustments.

3. How can I stay motivated to stick to my financial goals?

Set clear and achievable short-term and long-term goals. Regularly review your progress and celebrate small victories. Keeping the end goal in mind will help maintain motivation.

4. What is the snowball method for debt repayment?

The snowball method involves paying off your smallest debts first while making minimum payments on larger debts. Once a small debt is paid off, move to the next smallest. This method helps build momentum.

5. How much should I allocate to my emergency fund?

Aim to save three to six months’ worth of living expenses. This amount should cover essential expenses in case of unexpected events like job loss or medical emergencies.

6. How often should I review my investment portfolio?

Review your investment portfolio at least once a year, or more frequently if there are significant changes in your financial situation or the market. Adjust your strategy as needed to align with your goals.

7. What should I do if I find it difficult to cut expenses?

Start by identifying non-essential expenses that can be reduced or eliminated. Look for cheaper alternatives for essential services and consider lifestyle changes that can lead to savings.

Set up automatic transfers to your savings account. Treat savings as a non-negotiable expense in your budget to ensure consistent contributions.

9. Is it necessary to consult a financial advisor?

While not necessary, consulting a financial advisor can provide professional insights and personalized strategies. It’s especially beneficial if you’re dealing with complex financial situations or have specific investment goals.

10. What should I do if I encounter setbacks?

Setbacks are a normal part of financial management. Reassess your budget and goals, make necessary adjustments, and continue moving forward. Stay focused on your long-term objectives.