Managing personal finances can often feel overwhelming, especially for beginners who are just starting their budgeting journey. At the core of effective financial management lies the structure of one’s bank accounts. Setting up the right bank account structure is crucial for tracking expenses, saving for future goals, and ensuring financial stability. This guide, ‘Bank Account Structures for Beginner Budgeters,’ aims to demystify the process and provide a clear, structured approach to organizing your bank accounts.

For many individuals, the concept of budgeting brings images of complex spreadsheets and endless calculations. However, the fundamental principle of budgeting can be simplified by focusing on how your bank accounts are organized. By creating specific accounts for different financial purposes, you can gain better visibility into your spending habits and make more informed financial decisions.

In this guide, we will explore various bank account structures that cater to different budgeting needs and lifestyle choices. Whether you’re a student managing a tight budget, a young professional saving for your first home, or a family striving to secure a comfortable future, understanding and implementing the right bank account setup is essential. We will cover the basics of bank account types, delve into the history of how these structures evolved, and provide practical advice on how to tailor them to suit your personal financial goals.

Technical History of Bank Account Structures

Early Banking and the Evolution of Account Types

The concept of banking dates back to ancient civilizations, where merchants offered loans to farmers and traders who carried goods between cities. Fast forward to medieval times, and we see the rise of more structured financial institutions in Europe, particularly in Italy. These early banks provided a range of services, including the safekeeping of deposits and the facilitation of money transfers.

Initially, bank accounts were simple ledgers where deposits and withdrawals were recorded. Over time, as commerce expanded and economies grew more complex, so too did the need for different types of accounts. By the 19th century, with the industrial revolution in full swing, banks began to offer a variety of accounts to meet the diverse needs of their customers. This period saw the emergence of savings accounts, checking accounts, and other specialized accounts designed to cater to specific financial functions.

The Rise of Personal Banking

The 20th century marked a significant shift in banking with the introduction of personal banking services. As economies grew and personal wealth increased, banks started to see individuals as a major customer base. This led to the development of more tailored banking products, including personal checking accounts that facilitated the easy management of daily expenses and savings accounts that encouraged the accumulation of wealth over time.

During this time, technological advancements played a crucial role in transforming banking services. The introduction of computers revolutionized how banks maintained account records, leading to more efficient and accurate account management. This technological leap also paved the way for the development of automated teller machines (ATMs) in the 1960s, which provided customers with unprecedented access to their funds.

The Digital Revolution and Modern Bank Account Structures

The late 20th and early 21st centuries witnessed the digital revolution, which fundamentally changed the landscape of banking. The advent of the internet and mobile technology gave rise to online and mobile banking, allowing customers to manage their accounts from the comfort of their homes. This era also saw the introduction of electronic funds transfers, enabling instantaneous money movement between accounts.

With these technological advancements, banks began to offer a wider range of account options designed to meet specific financial goals. High-yield savings accounts, money market accounts, and certificates of deposit (CDs) became popular choices for individuals looking to maximize their savings. Additionally, the concept of sub-accounts gained traction, allowing customers to create dedicated funds within a single account for specific purposes, such as emergency savings, travel funds, or bill payments.

Modern Trends in Bank Account Structures

Today, the banking industry continues to evolve, driven by innovation and changing consumer needs. One of the key trends is the emphasis on financial literacy and empowerment. Banks are increasingly offering educational resources and tools to help customers better understand and manage their finances. This shift is particularly beneficial for beginner budgeters who may feel overwhelmed by the complexities of financial management.

Another notable trend is the rise of fintech companies, which have introduced new banking models that challenge traditional structures. These digital-first platforms often offer unique features, such as automated budgeting tools, round-up savings programs, and personalized financial advice, making it easier for individuals to achieve their financial goals.

In conclusion, the history of bank account structures is one of continuous evolution, shaped by technological advancements, economic changes, and the ever-evolving needs of consumers. By understanding this history, beginner budgeters can gain valuable insights into how to effectively manage their finances and set themselves up for a secure financial future.

Bank Account Structures for Beginner Budgeters

Bank Account Structures for Beginner Budgeters

Managing personal finances can be daunting for many individuals, especially those new to budgeting. One essential step in taking control of your financial future is understanding how to structure your bank accounts effectively. This guide will walk you through different bank account structures and provide practical tips for beginner budgeters.

1. Understanding the Basics

Before diving into specific account structures, it’s crucial to understand the types of accounts available:

Checking Account: A basic account for daily transactions, such as paying bills and making purchases.

Savings Account: An account designed to help you save money and earn interest over time.

Money Market Account: A type of savings account with higher interest rates but typically requires a higher minimum balance.

Certificate of Deposit (CD): A savings product with a fixed interest rate and fixed date of withdrawal, known as the maturity date.

For those just starting, a simple structure with two accounts can suffice:

Primary Checking Account: Use this for all your income and everyday expenses.

Primary Savings Account: Allocate a portion of your income to this account for emergencies and short-term savings goals.

This structure is easy to manage and provides a clear distinction between spending and saving.

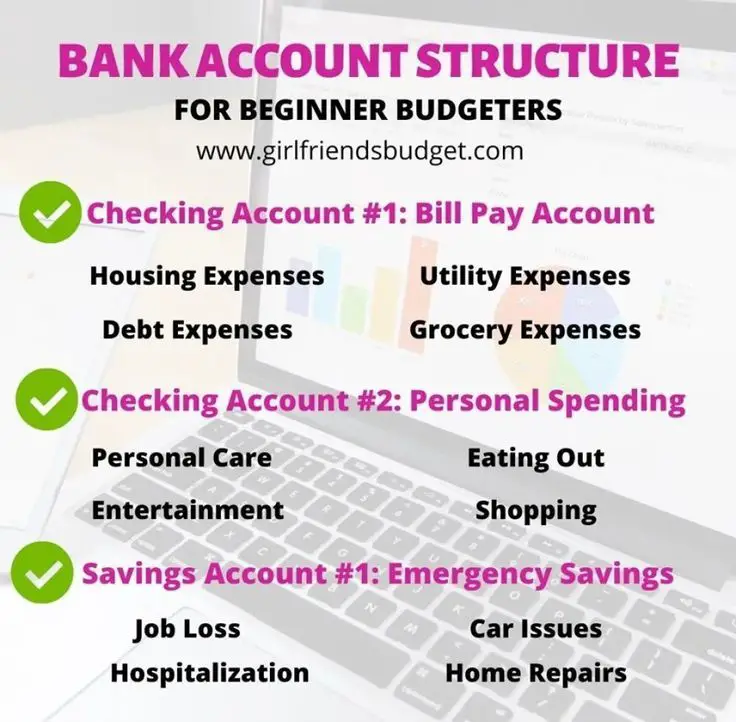

3. The Three-Bucket System

As you become more comfortable with budgeting, you might want to explore the three-bucket system:

Everyday Checking Account: For regular expenses such as groceries, utilities, and transportation.

Emergency Savings Account: Aim to save 3-6 months of living expenses for unexpected events.

Goal-Specific Savings Account: Use this for specific financial goals like vacations, a new car, or home improvement.

This structure helps you allocate funds effectively and keeps your savings organized.

4. The Envelope System

The envelope system is a cash-based method where you allocate money into different envelopes for specific expenses. However, you can adapt this to a digital format:

Multiple Checking Accounts: Open separate accounts for fixed expenses, flexible spending, and savings goals.

This system allows for detailed tracking and control over spending in each category.

5. Automate Your Savings

Automating your savings can be a game-changer for beginner budgeters. Set up automatic transfers from your checking to your savings account on payday. This ensures that you consistently save without having to think about it.

6. Regularly Review and Adjust

Your financial situation and goals will change over time. It’s crucial to regularly review your bank account structures and make adjustments as needed. Assessing your spending habits and savings goals every few months can help you stay on track.

7. Use Technology to Your Advantage

Many banks offer online tools and mobile apps to help manage your accounts. Use these tools to track your spending, set savings goals, and view account balances in real-time. Budgeting apps like Mint or You Need A Budget (YNAB) can also provide valuable insights.

8. Seek Professional Advice

If you’re feeling overwhelmed, consider seeking advice from a financial advisor. They can help you create a personalized bank account structure that aligns with your financial goals and circumstances.

9. Stay Informed

Financial literacy is key to effective budgeting. Take time to educate yourself about personal finance topics such as interest rates, credit scores, and investment options. The more you know, the better equipped you’ll be to make informed decisions.

10. Be Patient and Persistent

Building a solid financial foundation takes time and effort. Be patient with yourself and remain persistent in your budgeting efforts. Over time, you’ll develop healthier financial habits and gain confidence in managing your money.

The number of accounts you should have depends on your financial goals and personal preferences. Many people find that having at least a checking and savings account is a good start.

2. What is the best way to use a checking account?

A checking account should be used for everyday expenses and transactions. It’s where your income is deposited and where you’ll pay most of your bills from.

3. How much should I keep in my savings account?

Aim to save at least 3-6 months’ worth of living expenses in your savings account as an emergency fund. However, this amount can vary based on your personal circumstances.

4. What is the envelope system?

The envelope system is a budgeting method where you allocate a set amount of cash into different envelopes for specific spending categories, helping you control and track your expenses.

5. Can I automate savings in a digital envelope system?

Yes, many banks and budgeting apps allow you to set up automatic transfers to different accounts, mimicking the envelope system digitally.

6. Should I use a budgeting app?

Budgeting apps can be incredibly helpful for tracking spending and setting financial goals. Consider using one if you prefer digital solutions.

7. How often should I review my bank account structure?

It’s a good idea to review your bank account structure every few months or whenever there’s a significant change in your financial situation.

8. What if I’m not meeting my savings goals?

If you’re not meeting your savings goals, review your budget to identify areas for improvement. Consider reducing discretionary spending or finding ways to increase your income.

9. Is it necessary to have a money market account?

A money market account isn’t necessary for everyone, but it can be a good option if you’re looking for a higher interest rate and can maintain the minimum balance required.

10. How can I get help with budgeting?

If you’re struggling with budgeting, consider seeking advice from a financial advisor or using online resources and courses to improve your financial literacy.