Money doesn’t come with an instruction manual. Most of us grow up learning math, science, and history—but very few of us are taught how to manage money. That’s why so many people enter adulthood unprepared, making expensive mistakes that can take years (or even decades) to undo.

The good news? Money isn’t as complicated as it sometimes feels. In fact, there are timeless financial principles that can guide you toward stability, security, and freedom. If you can master these six simple rules by the time you turn 30, you’ll be far ahead of the majority of people.

Think of these as financial guardrails: they don’t restrict you, they protect you. They make sure you’re on track while still giving you freedom to enjoy life.

Here are the six rules we’ll dive deep into:

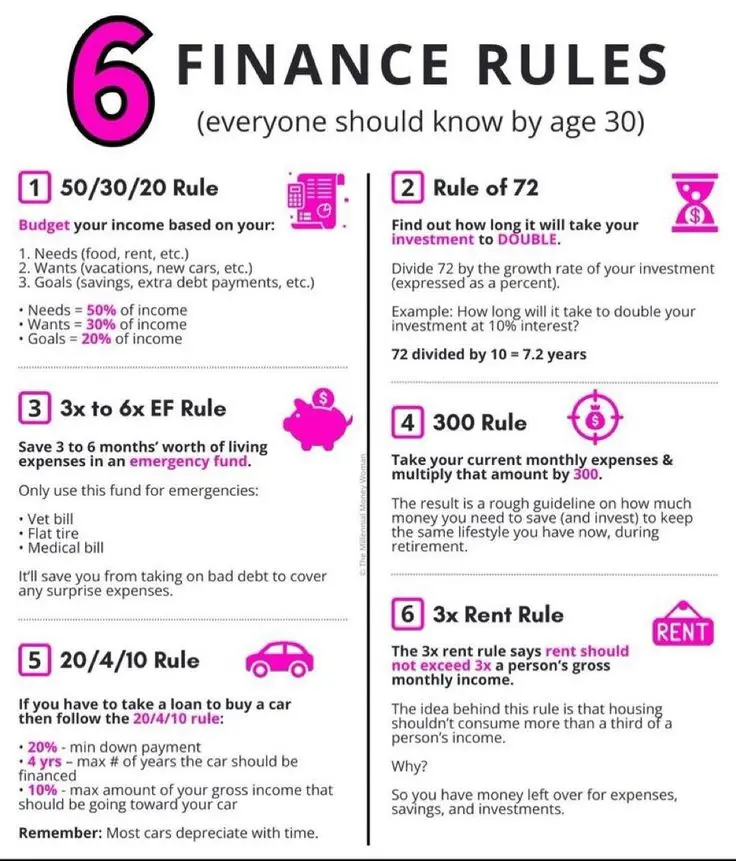

- The 50/30/20 Rule – A simple system for budgeting.

- The Rule of 72 – A shortcut to understand compound growth.

- The 3–6 Months Emergency Fund Rule – Your financial safety net.

- The 300 Rule for Retirement – How much you’ll need to retire.

- The 20/4/10 Car Rule – A guideline for buying cars wisely.

- The 3x Rent Rule – Housing costs shouldn’t overwhelm your budget.

Let’s break each one down.

Rule 1: The 50/30/20 Rule

This is one of the simplest, most effective ways to budget without getting lost in spreadsheets.

- 50% of income → Needs

Essentials like rent, groceries, utilities, insurance, and transportation. - 30% of income → Wants

Fun money: travel, restaurants, concerts, subscriptions, and shopping. - 20% of income → Goals

Savings, investments, debt payoff, and building financial security.

Why This Rule Works

- Keeps your lifestyle in check.

- Ensures you’re saving, not just spending.

- Offers balance—you enjoy today while building for tomorrow.

Example

Let’s say you earn $3,000 per month after taxes:

- Needs = $1,500

- Wants = $900

- Goals = $600

If you stick to this, in one year you’ll save $7,200—even if you’ve never saved before.

Variations

- If you live in a high-cost city (like New York or Tokyo), you might adjust to 60/20/20.

- If you want to build wealth faster, try 40/30/30.

Case Study: James

James earned $4,000/month but spent nearly everything. Once he applied the 50/30/20 rule, he cut down eating out, redirected $800/month toward investments, and within three years built a $30,000 portfolio.

Rule 2: The Rule of 72

This rule is a mental shortcut to understand the power of compound interest.

Formula:

72 ÷ Interest Rate (%) = Years to Double Investment

Example

If your investment grows at 10% annually:

72 ÷ 10 = 7.2 years to double.

So, if you invest $10,000 at age 25:

- At 32, it grows to ~$20,000.

- At 39, ~$40,000.

- At 46, ~$80,000.

- At 53, ~$160,000.

That’s the power of compounding.

Why This Rule Matters

- Shows why starting early is crucial.

- Makes growth easy to visualize.

- Reminds you that time is more important than timing.

Case Study: Anna vs Mark

- Anna invests $10,000 at age 25 at 8% growth.

- Mark invests $10,000 at age 35 at the same rate.

By 65:

- Anna has ~$217,000.

- Mark has only ~$101,000.

Same money, same rate—but Anna started earlier.

Rule 3: The 3–6 Months Emergency Fund Rule

Life is unpredictable. Cars break down. Pets get sick. Jobs disappear. That’s why you need a cushion.

The Rule

Save 3–6 months of living expenses in a safe, accessible account (like a high-yield savings account).

- 3 months if you’re single, low expenses, stable job.

- 6 months (or more) if you have dependents, high expenses, or unstable income.

What Counts as an Emergency?

- Car repair

- Vet bill

- Medical bill

- Job loss

What Doesn’t Count

- New iPhone

- Vacation

- Concert tickets

Example

If your expenses are $2,000/month:

- Minimum EF = $6,000

- Ideal EF = $12,000

Case Study: Emily

Emily lost her job unexpectedly. Because she had 5 months of expenses saved, she avoided debt, stayed calm, and found a new job without panic.

Rule 4: The 300 Rule for Retirement

Retirement planning feels overwhelming, but this rule gives a simple shortcut:

Formula:

Monthly Expenses × 300 = Retirement Goal

Example

If you spend $2,500/month:

$2,500 × 300 = $750,000 needed for retirement.

This is based on the 4% rule, which suggests you can safely withdraw ~4% of your investments yearly.

Why This Rule Works

- Focuses on expenses, not income.

- Adapts to your lifestyle choices.

- Gives a clear savings target.

Case Study: Daniel

Daniel spent $4,000/month. His retirement number = $1.2M. By investing $1,000/month starting at age 28, he’s on track to hit that number by his mid-60s.

Rule 5: The 20/4/10 Car Rule

Cars are one of the biggest money traps. They depreciate fast, yet many people overspend on them.

This rule keeps you safe:

- 20% down payment minimum.

- 4 years max loan term.

- 10% of gross income max for car expenses.

Why It Works

- Avoids being upside-down (owing more than the car is worth).

- Limits total interest paid.

- Keeps transportation affordable.

Example

If you earn $60,000/year ($5,000/month):

- Car expenses should be ≤ $500/month.

- With 20% down and 4-year financing, you’ll stay within budget.

Case Study: Sarah vs Mike

- Sarah followed the 20/4/10 rule. Bought a $20k car, paid it off in 4 years, and moved on.

- Mike ignored the rule. Bought a $45k truck with a 7-year loan. After 3 years, he still owed more than the truck was worth—and had no savings.

Rule 6: The 3x Rent Rule

Housing is the biggest expense for most people. The 3x rule keeps it reasonable.

The Rule

Your monthly income should be at least 3x your rent.

Or, flip it: your rent shouldn’t exceed ⅓ of your income.

Example

If you earn $4,500/month:

Rent should be ≤ $1,500.

Why This Rule Matters

- Keeps housing from swallowing your budget.

- Leaves room for savings and other expenses.

- Prevents “house poor” syndrome.

Exceptions

- High-cost cities: sometimes you’ll stretch to 40–50%.

- House-hacking: renting out rooms to offset costs.

- Living with roommates.

Case Study: Kevin

Kevin earned $3,600/month. Instead of renting a $1,800 luxury apartment, he chose a $1,200 place. That extra $600/month went into investments—building $7,200/year toward his future.

Conclusion: Your Financial Compass

These six rules aren’t random—they’re a framework for lifelong financial success:

- 50/30/20 Rule → Budget balance.

- Rule of 72 → Power of compounding.

- Emergency Fund Rule → Protection.

- 300 Rule → Retirement target.

- 20/4/10 Rule → Smart car buying.

- 3x Rent Rule → Affordable housing.

By age 30, mastering these rules will give you stability and momentum. They’re not cages—they’re freedom guidelines. They help you enjoy life today while ensuring you’re prepared for tomorrow.

Because money isn’t just about numbers—it’s about choices. The earlier you apply these principles, the more freedom you’ll have later.